Research · Nov 12, 2022

FOMC Minutes

Fatih Kansoy · Published in: Warwick Economics Research Papers, No. 1436

Plain-Language Summary

FOMC statements are released at the policy meeting, while minutes arrive later. The paper asks whether the later release still moves markets. If minutes only repeat information already known from the statement, they should not create large intraday market reactions.

The paper constructs monetary-policy surprise components from intraday futures data and studies market reactions around FOMC minutes releases. The design follows the high-frequency event-study logic used in monetary-policy surprise measurement: narrow windows reduce the chance that unrelated news drives the observed price changes.

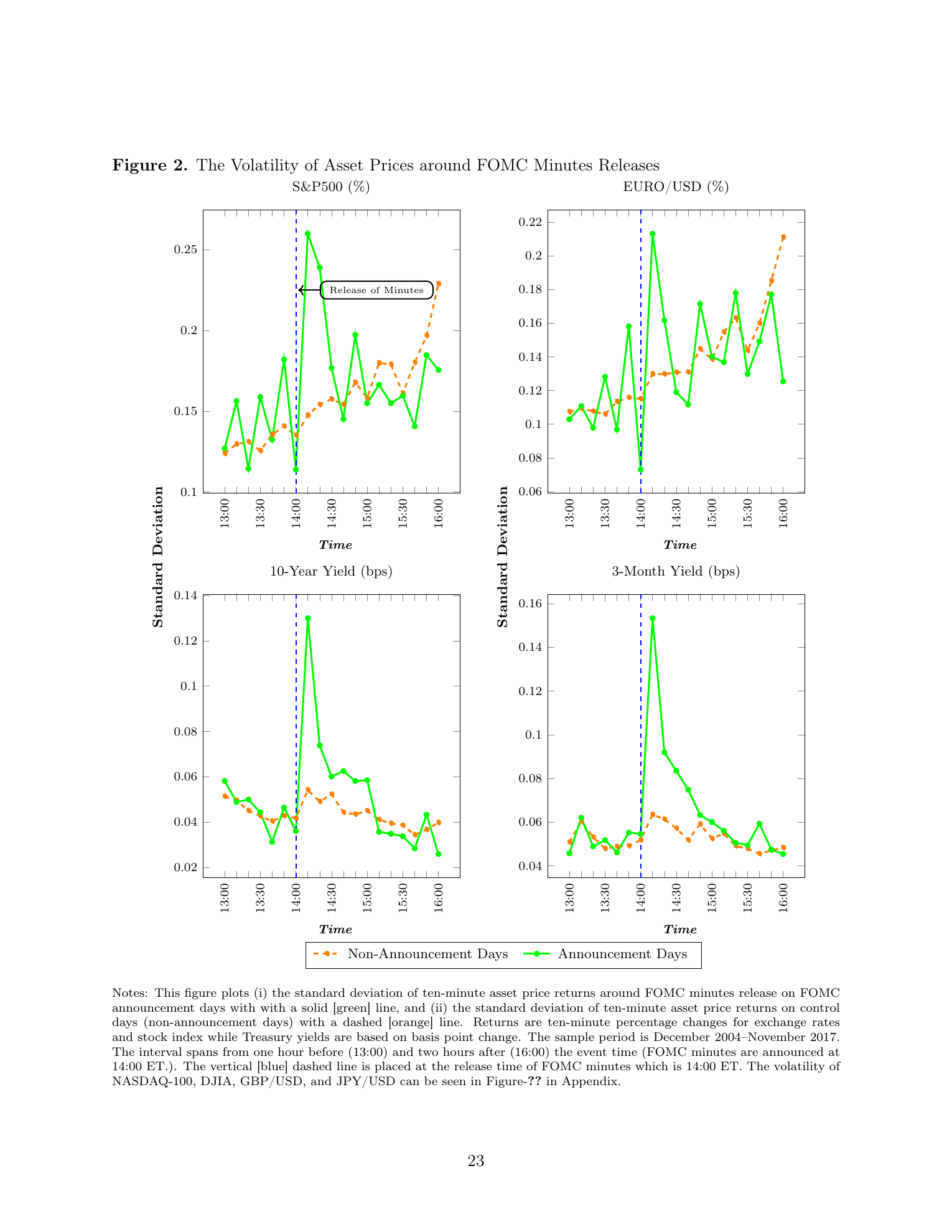

The results show that minutes releases are not neutral background documents. They raise volatility, generate significant asset-price responses, and become especially important during the zero lower bound period, when information about the future policy path mattered more than changes in the current policy rate.

Research Question

Do FOMC minutes contain new market-relevant information after the statement has already been released?

Why It Matters

The paper matters because central-bank communication is not a single announcement. Minutes may reveal discussion, balance of views, and future-path information that financial markets still price.

Data

The sample covers FOMC minutes and statement announcements from December 2004 to November 2017. It uses high-frequency US asset prices measured at ten-minute intervals, including stock markets, Treasury yields, and exchange rates.

Method

The paper constructs target and path surprises using intraday Fed funds futures data, then estimates event-study responses of asset prices and volatility around minutes releases. It compares conventional and zero-lower-bound periods.

Contribution and Findings

Minutes raise volatility

The release of FOMC minutes induces higher-than-normal volatility across asset classes.

Markets respond quickly

Financial markets respond quickly and significantly to minutes surprises.

Responses differ by asset

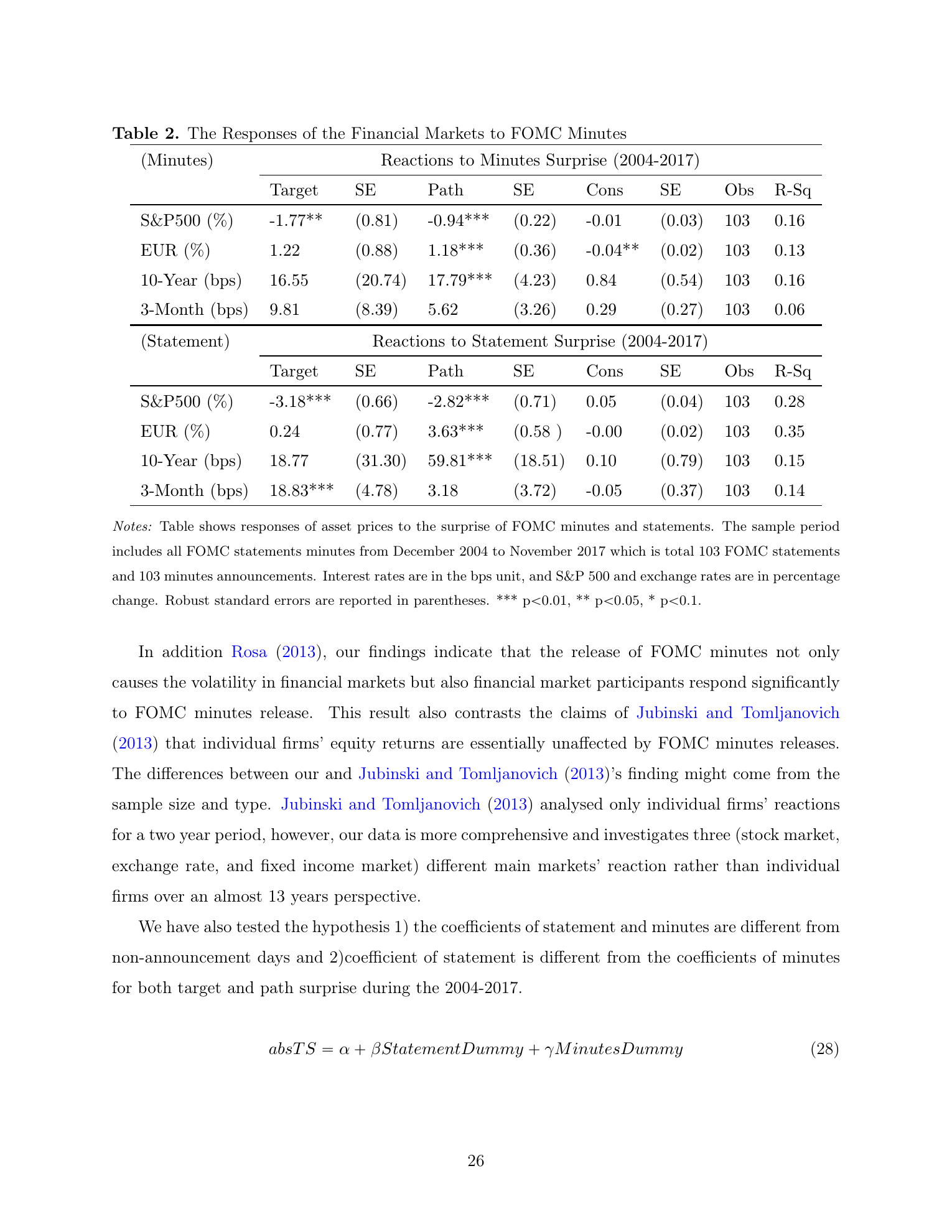

Stock markets, exchange rates, and longer-term rates respond differently to target and path components.

ZLB period is stronger

Volatility and responses increase during the zero lower bound period, when path information is especially valuable.

The paper extends high-frequency monetary-policy surprise measurement to FOMC minutes and shows that minutes can be an important source of central-bank communication surprise.

Figures and Tables

Results Table

Key results from the paper

| Evidence | Result | Interpretation |

|---|---|---|

| Volatility | Higher than normal on minutes release days | Minutes contain information markets still process. |

| Asset-price response | Quick and significant responses across several markets | The release is a market event. |

| Target surprise | Stock-market response is negative and significant in the paper's discussion | Current-rate information still matters for equities. |

| Path surprise | Exchange-rate and ten-year-rate responses are positive and significant | Future-path information is a central channel. |

Scope and Limits

The paper's methods and terminology reflect the 2022 working-paper version. The event-study design identifies high-frequency market reactions, not longer-run macroeconomic effects.

Selected References

- Blinder, A. S., Ehrmann, M., Fratzscher, M., De Haan, J., and Jansen, D.-J. 2008. Central bank communication and monetary policy.

- Cook, T. and Hahn, T. 1989. The effect of changes in the federal funds rate target on market interest rates.

- Gurkaynak, R. S., Sack, B., and Swanson, E. T. 2005. Do actions speak louder than words?

- Kuttner, K. N. 2001. Monetary policy surprises and interest rates.

- Rosa, C. 2013. The financial market effect of FOMC minutes.

How to Cite

Use the copy buttons for quick citation text, or open the raw BibTeX and RIS records in your browser.

APA

Kansoy, F. (2022). FOMC Minutes: As a Source of Monetary Policy Surprise. Warwick Economics Research Papers, No. 1436. https://fatih.ai/research/fomc_minutes/Chicago

Kansoy, Fatih. 2022. "FOMC Minutes: As a Source of Monetary Policy Surprise." Warwick Economics Research Papers, No. 1436. https://fatih.ai/research/fomc_minutes/.Harvard

Kansoy, F. 2022, 'FOMC Minutes: As a Source of Monetary Policy Surprise', Warwick Economics Research Papers, No. 1436, available at: https://fatih.ai/research/fomc_minutes/.BibTeX

@article{kansoy2022fomc,

title = {FOMC Minutes: As a Source of Monetary Policy Surprise},

author = {Fatih Kansoy},

journal = {Warwick Economics Research Papers, No. 1436},

year = {2022},

url = {https://fatih.ai/minutes.pdf}

}RIS

TY - JOUR

TI - FOMC Minutes: As a Source of Monetary Policy Surprise

AU - Fatih Kansoy

PY - 2022

T2 - Warwick Economics Research Papers, No. 1436

UR - https://fatih.ai/minutes.pdf

ER -