Summary

Does ESG protect firms in bad times, or make them more exposed to rate news? This paper finds a two-sided answer: high-ESG firms are relatively protected from contractionary target surprises, yet they become more sensitive to forward-guidance shocks because sustainability-oriented cash flows behave like longer-duration assets.

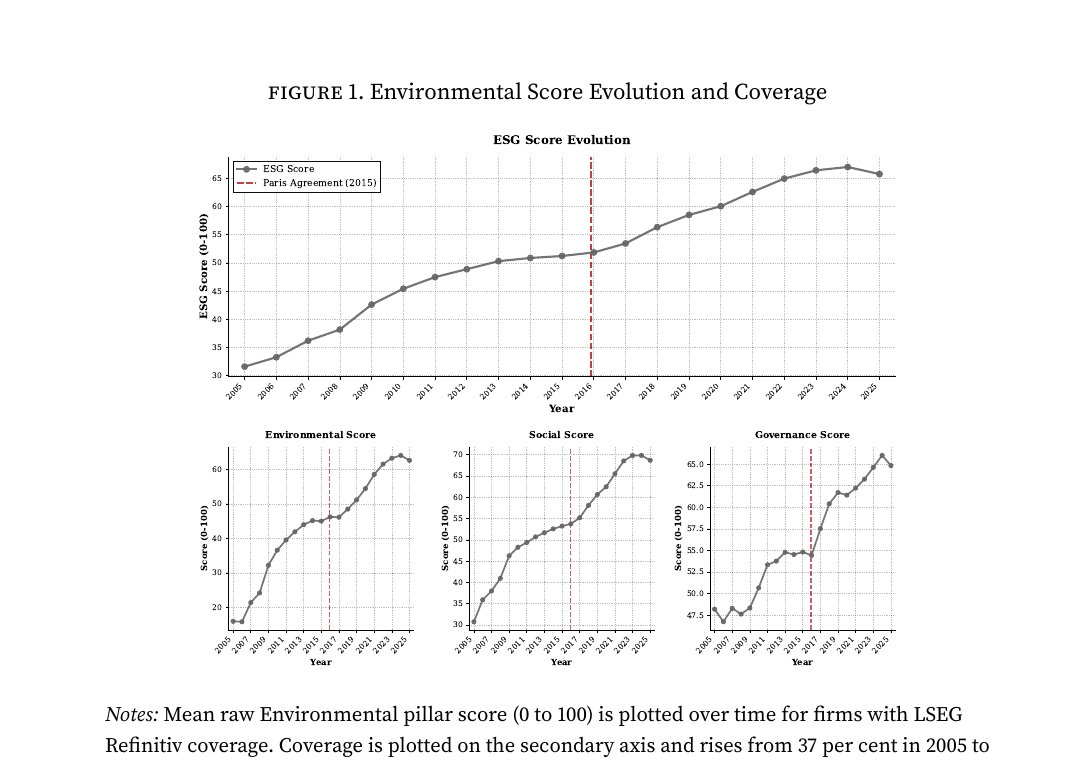

The striking result is that this relationship flips around the Paris Agreement. What looks like a stable ESG premium is actually regime-dependent monetary transmission, shaped by investor preferences and the depth of sustainable-finance markets rather than by a fixed green-firm technology.