Summary

Can international monetary spillovers be measured in real time when foreign cash markets are closed during FOMC announcements? Using US-traded country ETFs as a price-discovery venue, this paper shows that they can, and that a typical contractionary Fed surprise destroys about $280 billion in foreign equity value within thirty minutes.

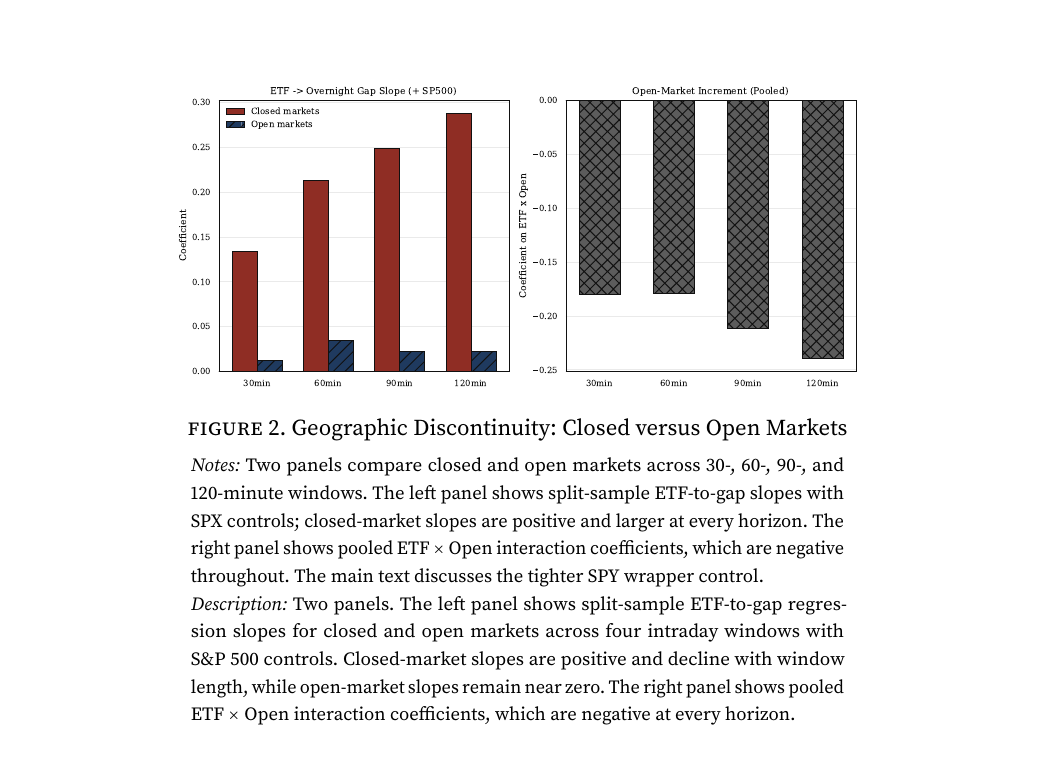

The effect appears in every country examined, regardless of exchange-rate regime, development level, or capital-account openness. The identification hinge is the geographic discontinuity below: ETF returns line up with overnight gaps for closed markets, but not for markets already open, which is exactly what the real-time spillover design requires.