Research · Feb 1, 2026

The Immediate Global Impact of US Monetary Policy

Fatih Kansoy · Published in: University of Oxford Department of Economics Discussion Papers

Plain-Language Summary

The paper studies what happens to foreign equity wealth at the exact moment US monetary policy news is released. The empirical difficulty is timing: many foreign cash equity markets are closed when FOMC announcements arrive, so daily local-index studies mix immediate repricing with overnight news, exchange-rate movement, and delayed market opening.

The solution is to use US-traded country ETFs. These trade during the FOMC window even when the underlying local market is closed. That makes it possible to measure the foreign-country response in the same narrow window in which the US policy surprise is measured.

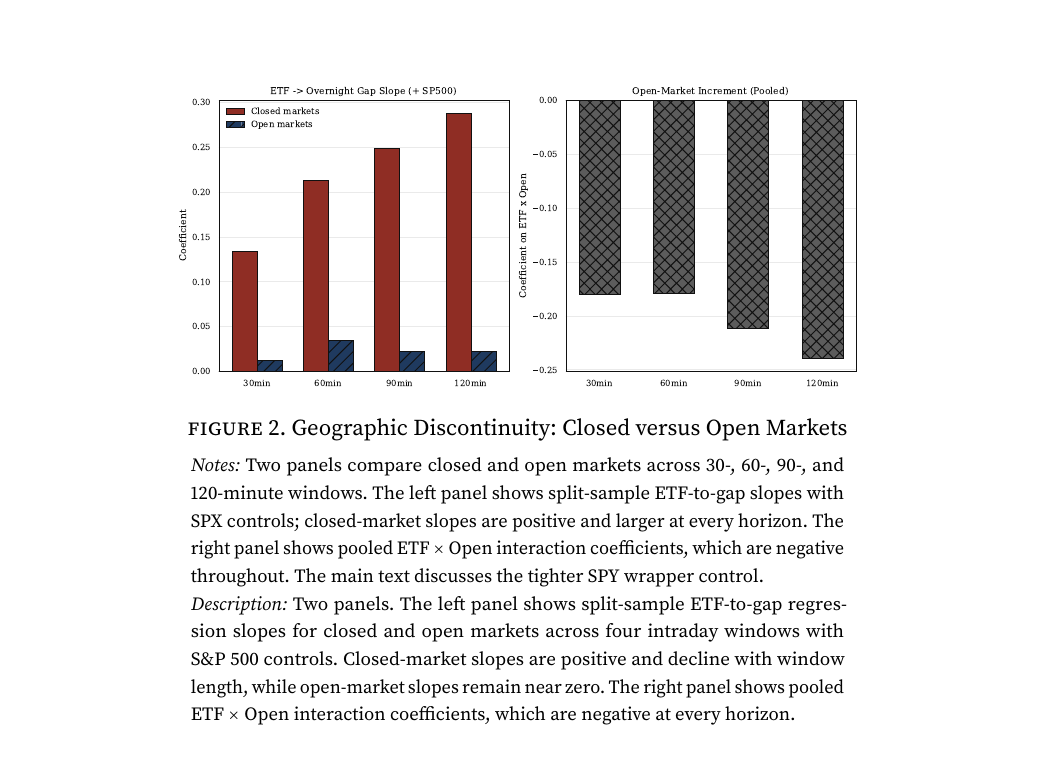

The key design check is geographic. ETF returns during the announcement window predict the next-open local-index gap for closed markets, but not for markets that were already open. That pattern supports the interpretation that the ETF is revealing the immediate foreign-market repricing that would otherwise be hidden until the local market opens.

Research Question

How large is the immediate global equity-market response to US monetary policy when foreign markets are measured in the same high-frequency window as the FOMC surprise?

Why It Matters

The paper changes the measurement problem in international monetary spillovers. If foreign markets are closed, daily local-index responses can miss the immediate repricing that investors observe through US-traded instruments. Measuring the response with country ETFs makes the spillover visible within minutes rather than at the next trading day.

Data

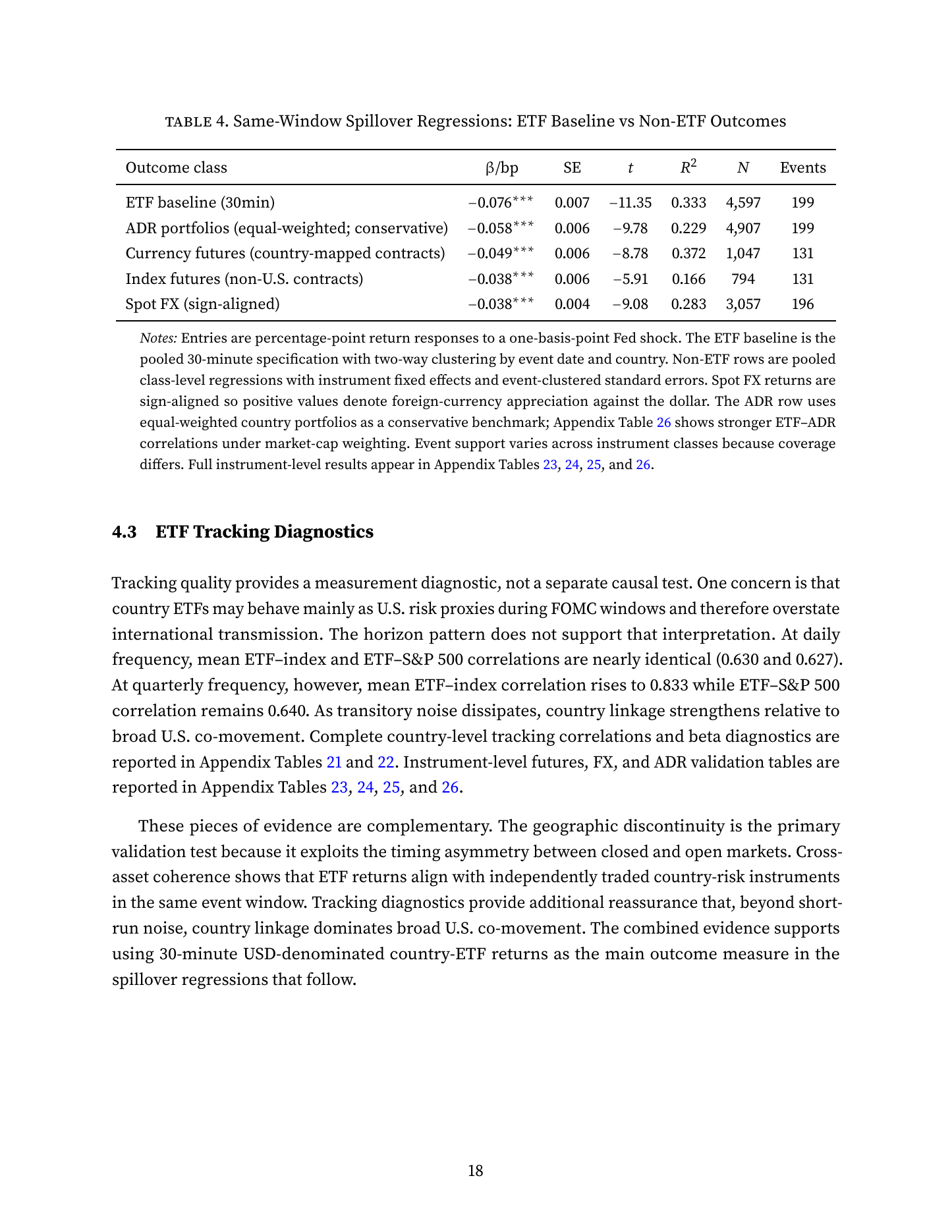

The paper uses a 37-country ETF panel, scheduled and unscheduled FOMC events, and high-frequency market data. The country ETF estimation sample contains tens of millions of one-minute observations, matched to FOMC surprises measured in a narrow announcement window.

Method

The empirical design combines high-frequency event studies around FOMC announcements with country ETF returns. A geographic discontinuity validates the approach by comparing closed and open foreign cash markets. Cross-country regressions then study the magnitude and persistence of the immediate spillover.

Contribution and Findings

Spillovers are broad

The country-level point estimates are negative in every adequate-coverage country in the paper's panel.

The wealth effect is large

A one-standard-deviation contractionary surprise reprices roughly $150-$300 billion in non-US equity wealth within thirty minutes.

The response is not only FX

Roughly half of the repricing reflects local-currency equity movement rather than exchange-rate adjustment alone.

Observable characteristics explain little

Trade openness, exchange-rate regime, and ratings shift sensitivity at the margin but explain only a modest share of cross-country variation.

The paper provides a way to observe global monetary spillovers in the same high-frequency window used to identify US policy news. It shows that previous designs can understate the size and commonality of global equity repricing when foreign markets are closed.

Figures and Tables

Results Table

Key results from the paper

| Evidence | Result | Interpretation |

|---|---|---|

| ETF design | ETF returns predict next-open local-index gaps for closed markets | The ETF response captures delayed local-market repricing. |

| Country panel | Negative point estimates in every adequate-coverage country | The spillover is broad rather than concentrated in a few markets. |

| Wealth effect | $150-$300 billion repriced within thirty minutes | Immediate foreign equity wealth effects are large. |

| Currency decomposition | Roughly half is local-currency equity repricing | The effect is not just exchange-rate translation. |

Scope and Limits

The ETF design observes liquid US-traded country funds and is strongest where ETF coverage is adequate. The paper measures financial-market repricing, not the full macroeconomic transmission to output or inflation.

Selected References

- Altavilla, C., Giannone, D., and Modugno, M. 2017. Low-frequency effects of macroeconomic news on government bond yields.

- Ammer, J., Vega, C., and Wongswan, J. 2010. International transmission of US monetary policy shocks.

- Gurkaynak, R. S., Sack, B., and Swanson, E. 2005. Do actions speak louder than words?

- Kuttner, K. N. 2001. Monetary policy surprises and interest rates.

- Hausman, J. and Wongswan, J. Global asset prices and FOMC announcements.

How to Cite

Use the copy buttons for quick citation text, or open the raw BibTeX and RIS records in your browser.

APA

Kansoy, F. (2025). The Immediate Global Impact of US Monetary Policy. University of Oxford Department of Economics Discussion Papers. https://fatih.ai/research/immediate_global_impact_us_monetary_policy/Chicago

Kansoy, Fatih. 2025. "The Immediate Global Impact of US Monetary Policy." University of Oxford Department of Economics Discussion Papers. https://fatih.ai/research/immediate_global_impact_us_monetary_policy/.Harvard

Kansoy, F. 2025, 'The Immediate Global Impact of US Monetary Policy', University of Oxford Department of Economics Discussion Papers, available at: https://fatih.ai/research/immediate_global_impact_us_monetary_policy/.BibTeX

@article{kansoy2025global,

title = {The Immediate Global Impact of US Monetary Policy},

author = {Fatih Kansoy},

journal = {University of Oxford Department of Economics Discussion Papers},

year = {2025},

url = {https://fatih.ai/etf.pdf}

}RIS

TY - JOUR

TI - The Immediate Global Impact of US Monetary Policy

AU - Fatih Kansoy

PY - 2025

T2 - University of Oxford Department of Economics Discussion Papers

UR - https://fatih.ai/etf.pdf

ER -