Summary

Do firms with stronger environmental performance respond differently to monetary policy, and does it matter which part of the yield curve moves? Using high-frequency identification around FOMC announcements from 2005 to 2025, this paper shows that the key heterogeneity sits in forward-guidance or path shocks, not in current-rate shocks.

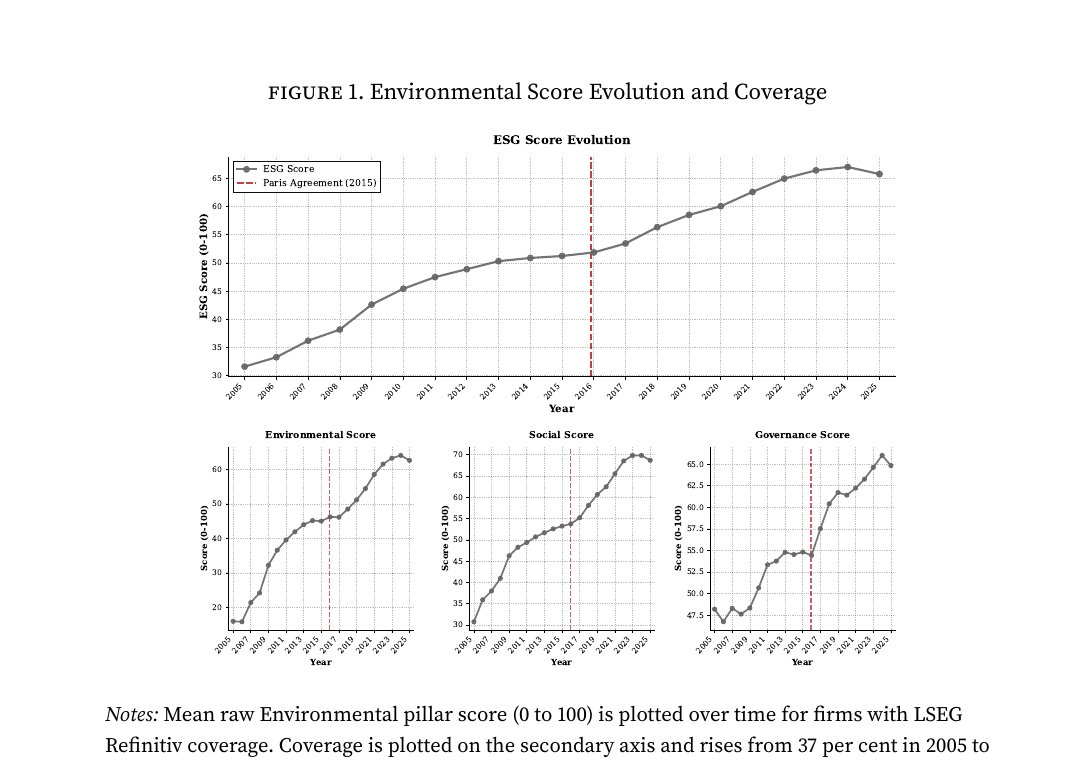

Before the Paris Agreement, greener firms were markedly more vulnerable to path shocks; after 2015 that vulnerability attenuates sharply, consistent with deeper green-finance markets improving hedging capacity. The broader message is that environmental transmission is not fixed: it evolves with financial-market structure and access.