Research · Oct 1, 2025

Monetary Policy Transmission and Environmental Performance

Fatih Kansoy and Dominykas Stasiulaitis · Published in: University of Oxford Department of Economics Discussion Papers

Plain-Language Summary

The paper asks whether environmental characteristics change how firms respond to monetary policy. The answer depends on which part of monetary policy moves. Current-rate or target surprises and longer-horizon path surprises are economically different, and the paper shows that environmental heterogeneity is much clearer in the path channel.

The interpretation is tied to horizon and financing structure. Greener or higher-environmental-score firms can be more exposed to long-horizon discount-rate news when their expected cash flows, investment horizons, or investor bases make them sensitive to forward guidance. That exposure is not fixed across time.

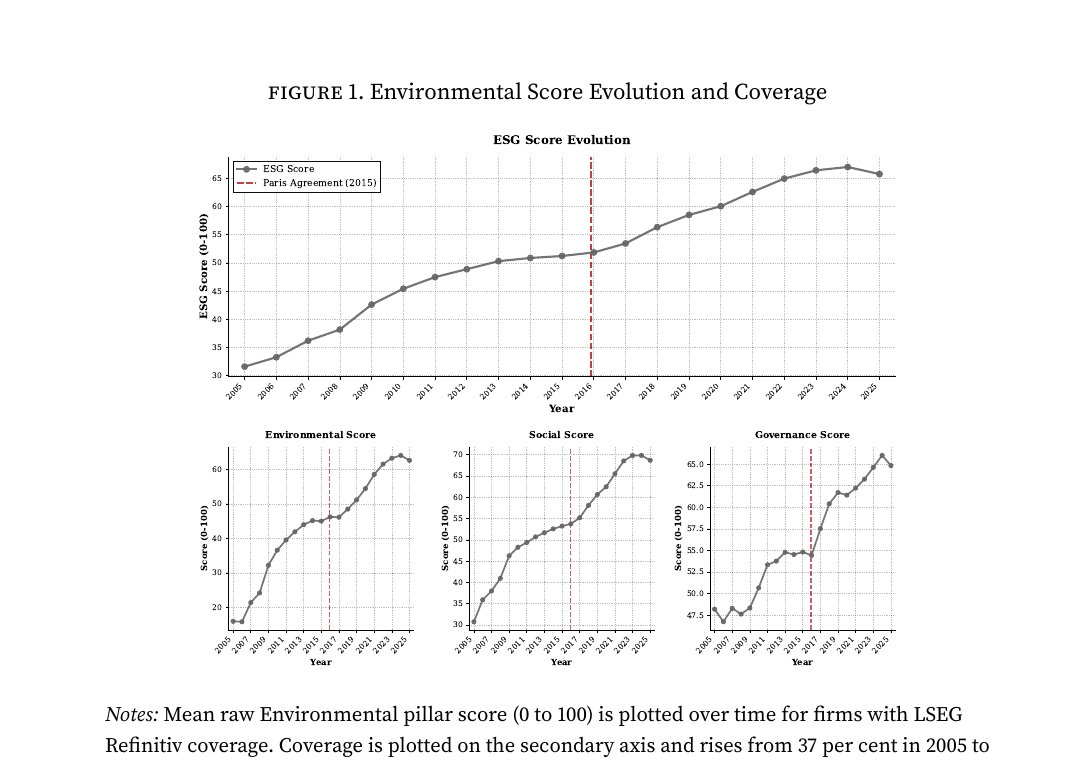

The post-2015 attenuation is central. Around the period in which green finance and climate-aware capital markets deepened, the pre-Paris vulnerability to path shocks becomes much weaker in the expanding-coverage sample. The paper is careful not to claim a single mechanism, but the pattern is consistent with improved hedging capacity and changing market structure.

Research Question

Do firms with stronger environmental performance respond differently to monetary policy, and does the answer depend on target versus path surprises?

Why It Matters

The paper connects climate finance to monetary transmission. If environmental performance changes the response to forward guidance, then green finance is not only a portfolio or disclosure issue; it also changes how monetary policy news is priced across firms.

Data

The study uses firm-level equity returns around FOMC announcements from 2005 to 2025, environmental and ESG scores, firm controls, and high-frequency target-path monetary policy surprises. The sample focuses on listed US firms with environmental score coverage.

Method

The paper estimates firm-level high-frequency announcement-window responses with industry-by-event fixed effects and firm controls. It decomposes monetary news into target and path channels and studies interactions with environmental performance across time and sample definitions.

Contribution and Findings

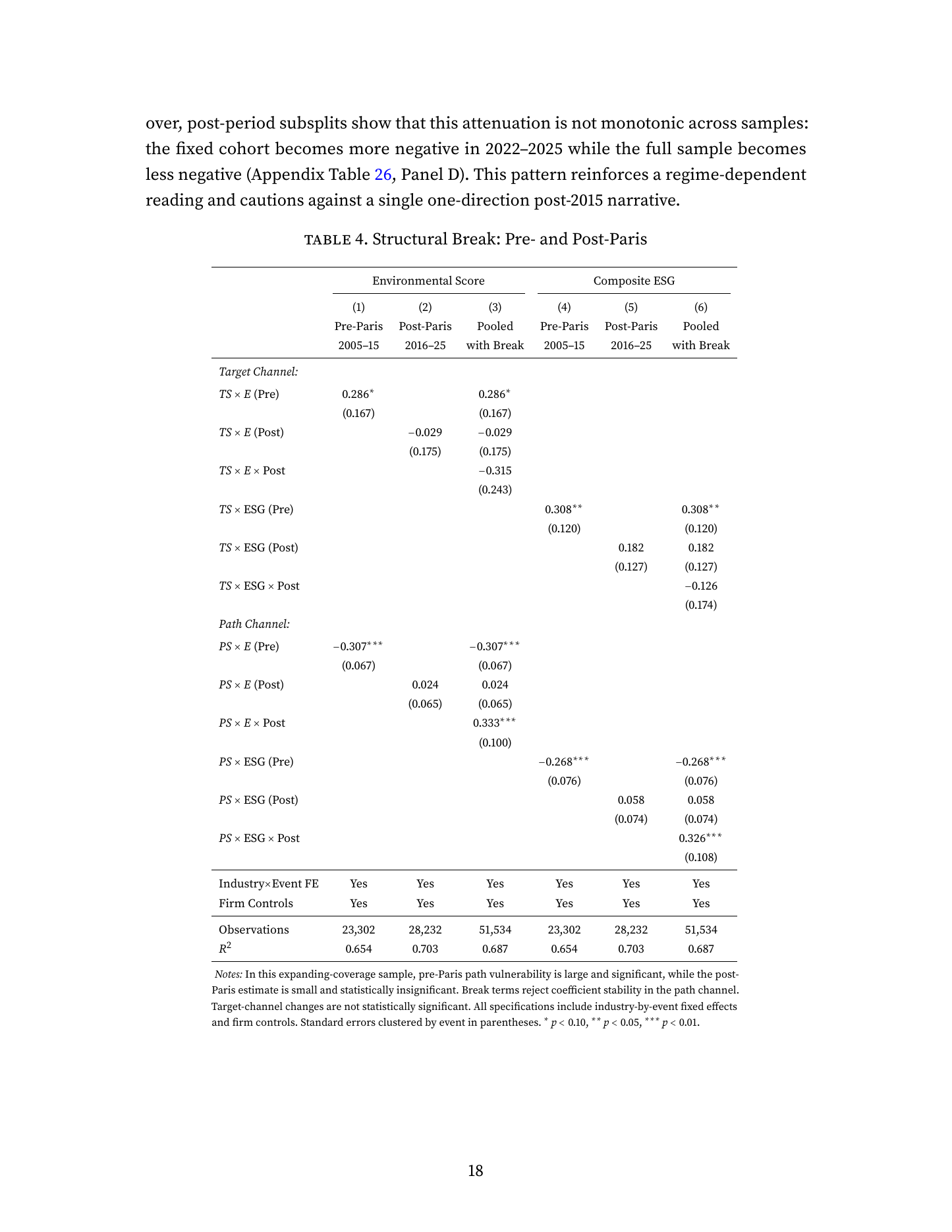

Path channel is central

Environmental heterogeneity is strongest for forward-guidance or path surprises, while the target-channel evidence is weaker and less stable.

Pre-Paris vulnerability

Before 2016, contractionary path surprises are associated with more negative announcement-window returns for higher-environmental-score firms.

Post-2015 attenuation

The path-channel vulnerability weakens sharply after 2015 in the expanding-coverage sample, though fixed-composition panels are more partial and imprecise.

Reduced-form scope

The paper documents reduced-form transmission patterns and does not claim to isolate a single structural mechanism.

The paper adds environmental performance as a time-varying dimension of monetary-policy transmission. It shows that the relevant heterogeneity can sit in forward guidance rather than current-rate news.

Figures and Tables

Results Table

Key results from the paper

| Evidence | Result | Interpretation |

|---|---|---|

| Target surprises | Moderation is weaker and less stable | Current-rate news is not where the main environmental heterogeneity appears. |

| Path surprises | Negative and significant interactions in the main specifications | Forward-guidance news is the central transmission channel. |

| Pre-2016 period | Higher environmental scores linked to larger negative responses to contractionary path surprises | Greener firms were more exposed to long-horizon policy news before the regime shift. |

| Post-2015 period | Attenuation in the expanding-coverage sample | The environmental transmission relationship evolves with financial-market structure. |

Scope and Limits

The evidence is based on listed firms with environmental score coverage and one main ESG data provider. The reduced-form estimates cannot fully separate duration, investor-clientele, disclosure, hedging, and financing mechanisms.

Selected References

- Bolton, P. and Kacperczyk, M. 2021. Do investors care about carbon risk?

- Bolton, P. and Kacperczyk, M. 2023. Global pricing of carbon-transition risk.

- Gurkaynak, R. S., Sack, B., and Swanson, E. 2005. Do actions speak louder than words?

- Gurkaynak, R. S., Karasoy-Can, H. G., and Lee, S. S. 2022. Stock market's assessment of monetary policy transmission.

- Swanson, E. Longer-run monetary policy surprise measurement used for path-channel interpretation.

How to Cite

Use the copy buttons for quick citation text, or open the raw BibTeX and RIS records in your browser.

APA

Kansoy, F., & Stasiulaitis, D. (2025). Monetary Policy Transmission and Environmental Performance: Firm-level Evidence from High-Frequency Identification. University of Oxford Department of Economics Discussion Papers. https://fatih.ai/research/monetary_policy_transmission_environmental_performance/Chicago

Kansoy, Fatih, and Dominykas Stasiulaitis. 2025. "Monetary Policy Transmission and Environmental Performance: Firm-level Evidence from High-Frequency Identification." University of Oxford Department of Economics Discussion Papers. https://fatih.ai/research/monetary_policy_transmission_environmental_performance/.Harvard

Kansoy, F., & Stasiulaitis, D. 2025, 'Monetary Policy Transmission and Environmental Performance: Firm-level Evidence from High-Frequency Identification', University of Oxford Department of Economics Discussion Papers, available at: https://fatih.ai/research/monetary_policy_transmission_environmental_performance/.BibTeX

@article{kansoy2025monetary,

title = {Monetary Policy Transmission and Environmental Performance: Firm-level Evidence from High-Frequency Identification},

author = {Fatih Kansoy and Dominykas Stasiulaitis},

journal = {University of Oxford Department of Economics Discussion Papers},

year = {2025},

url = {https://fatih.ai/esg.pdf}

}RIS

TY - JOUR

TI - Monetary Policy Transmission and Environmental Performance: Firm-level Evidence from High-Frequency Identification

AU - Fatih Kansoy

AU - Dominykas Stasiulaitis

PY - 2025

T2 - University of Oxford Department of Economics Discussion Papers

UR - https://fatih.ai/esg.pdf

ER -