Research · Jan 1, 2012

The Determinants of Net Interest Margin in the Turkish Banking Sector

Fatih Kansoy · Published in: Journal of BRSA Banking and Financial Markets, 6(2), 13-49

Plain-Language Summary

Net interest margin is a key banking-sector measure because it affects financial intermediation, credit conditions, and bank profitability. The paper asks which bank-specific, sector-specific, and macroeconomic factors explain margins in Turkey and whether ownership changes those relationships.

The evidence points to a combination of management quality, operating costs, credit risk, implicit interest payments, deposit growth, operational diversity, and inflation. Ownership is not a cosmetic classification; it changes how several determinants map into margins.

The policy message is direct. Lower margins are linked to better management efficiency and price stability. For banks, reducing operating costs and improving efficiency matter. For policymakers, inflation control supports stronger financial intermediation by reducing upward pressure on margins.

Research Question

What determines net interest margins in Turkey's commercial banking sector, and does bank ownership matter?

Why It Matters

Net interest margins affect the cost of intermediation and the efficiency of the banking system. Understanding ownership differences matters for regulation, competition policy, and financial stability.

Data

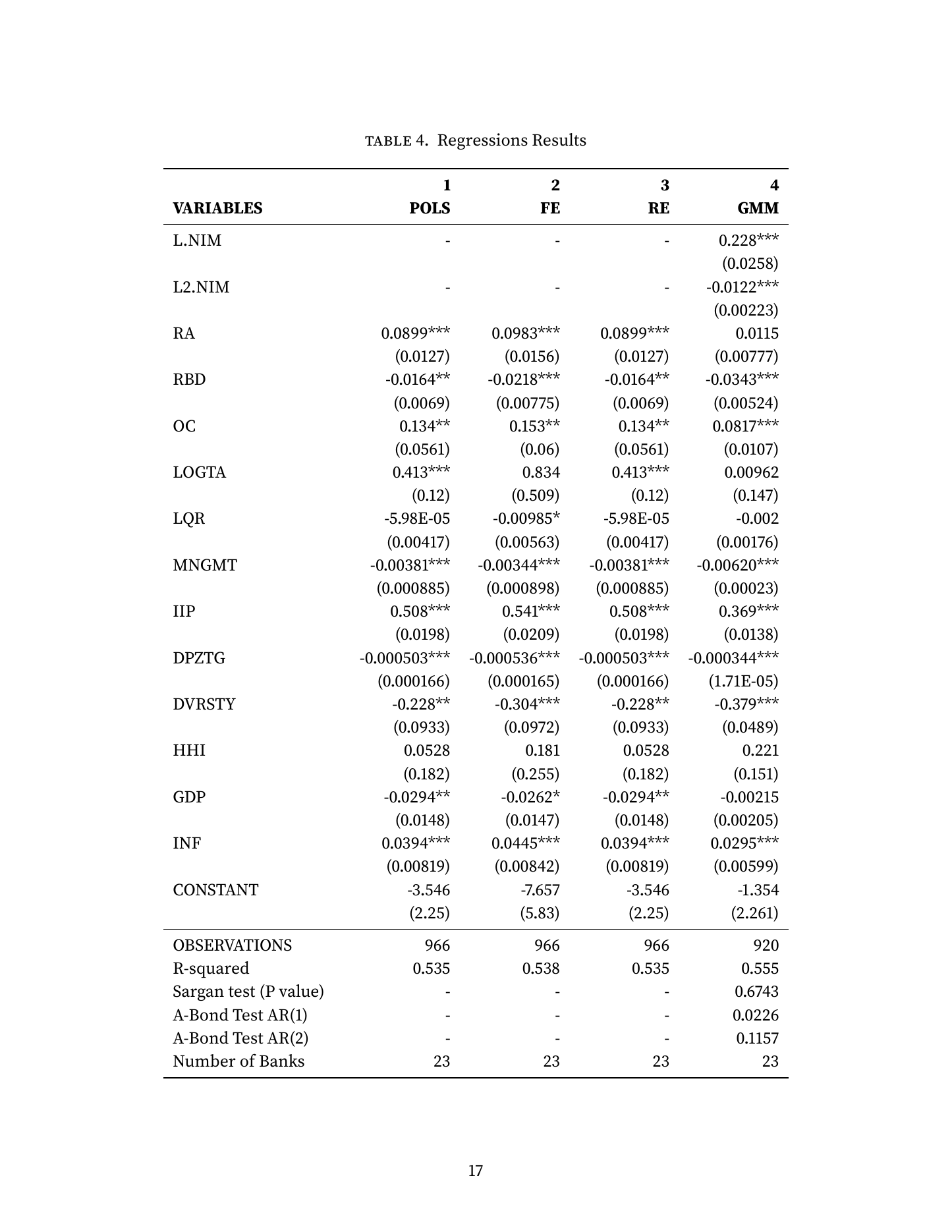

The paper uses quarterly bank-level data for 23 commercial banks in Turkey from the fourth quarter of 2001 to the first quarter of 2012. Bank-specific and industry-specific data come from the Banks Association of Turkey, and macroeconomic variables come from the Central Bank of the Republic of Turkey.

Method

The paper estimates pooled OLS, fixed-effects, random-effects, and dynamic GMM models. The empirical design allows determinants to vary across ownership groups and examines both bank-specific and macroeconomic drivers.

Contribution and Findings

Efficiency lowers margins

More efficient banks exhibit lower interest margins, consistent with better management quality improving intermediation.

Operating costs raise margins

Banks with higher costs pass part of those costs to clients through higher loan rates or lower deposit rates.

Inflation matters

Higher inflation is associated with higher net interest margins, while price stability contributes to lower margins.

Ownership matters

The effects of credit risk, size, concentration, and inflation vary across foreign-owned, state-controlled, and private banks.

The paper contributes bank-level evidence for Turkey and shows that ownership structure should not be ignored when modelling net interest margins.

Figures and Tables

Results Table

Key results from the paper

| Evidence | Result | Interpretation |

|---|---|---|

| Management efficiency | Efficient banks have lower margins | Better management can improve financial intermediation. |

| Operating costs | Higher costs raise margins | Banks pass operating costs to clients. |

| Inflation | Higher inflation raises margins | Price stability supports lower intermediation costs. |

| Ownership | Several determinants vary across ownership groups | Ownership structure matters for banking-sector analysis. |

Scope and Limits

The sample ends in 2012 and reflects Turkey's banking-sector structure during that period. The findings should be updated before drawing conclusions about the current banking system.

Selected References

- Ho, T. S. Y. and Saunders, A. 1981. The determinants of bank interest margins.

- Demirguc-Kunt, A. and Huizinga, H. 1999. Determinants of commercial bank interest margins and profitability.

- Saunders, A. and Schumacher, L. 2000. The determinants of bank interest rate margins.

- Fungacova, Z. and Poghosyan, T. 2011. Determinants of bank interest margins in Russia.

- Kasman, A., Tunc, G., Vardar, G., and Okan, B. 2010. Consolidation and commercial bank net interest margins.

How to Cite

Use the copy buttons for quick citation text, or open the raw BibTeX and RIS records in your browser.

APA

Kansoy, F. (2012). The Determinants of Net Interest Margin in the Turkish Banking Sector: Does Bank Ownership Matter? Journal of BRSA Banking and Financial Markets, 6(2), 13-49. https://fatih.ai/research/net_interest_margin_turkish_banking/Chicago

Kansoy, Fatih. 2012. "The Determinants of Net Interest Margin in the Turkish Banking Sector: Does Bank Ownership Matter?" Journal of BRSA Banking and Financial Markets, 6(2), 13-49. https://fatih.ai/research/net_interest_margin_turkish_banking/.Harvard

Kansoy, F. 2012, 'The Determinants of Net Interest Margin in the Turkish Banking Sector: Does Bank Ownership Matter?', Journal of BRSA Banking and Financial Markets, 6(2), 13-49, available at: https://fatih.ai/research/net_interest_margin_turkish_banking/.BibTeX

@article{kansoy2012determinants,

title = {The Determinants of Net Interest Margin in the Turkish Banking Sector: Does Bank Ownership Matter?},

author = {Fatih Kansoy},

journal = {Journal of BRSA Banking and Financial Markets, 6(2), 13-49},

year = {2012},

volume = {6},

number = {2},

pages = {13-49},

url = {https://fatih.ai/nim.pdf}

}RIS

TY - JOUR

TI - The Determinants of Net Interest Margin in the Turkish Banking Sector: Does Bank Ownership Matter?

AU - Fatih Kansoy

PY - 2012

T2 - Journal of BRSA Banking and Financial Markets, 6(2), 13-49

VL - 6

IS - 2

SP - 13

EP - 49

UR - https://fatih.ai/nim.pdf

ER -