Case studies · 2020

The Treasury basis trade and March 2020

Leveraged funds bet on a tiny gap between Treasury bonds and Treasury futures, and a dash for cash forced a rapid, disorderly unwind.

What happened

A trade too dull to explain

The cash-futures basis trade buys a Treasury bond, sells a Treasury futures contract against it, and pockets a spread of a few tens of basis points. Hedge funds run this every day. In the years running up to 2020, it grew enormously: hedge funds' total Treasury exposure rose by almost $1 trillion between 2017 and 2019 alone, as the arbitrage became more attractive and more crowded.

On the surface the trade looks close to riskless. A long position in the bond's price risk and a short position in the future's price risk mean that a rise or fall in interest rates affects both legs in opposite, roughly offsetting ways. What is left over, the basis, is a thin, usually stable gap between the cost of carrying the bond and what the futures market pays for that exposure. The whole business model, though, only works at very high leverage, financed almost entirely through overnight repo borrowing. A few tens of basis points is not an attractive return on its own; it becomes one only once magnified many times over on a small sliver of investor equity.

A safe haven that stops acting safe

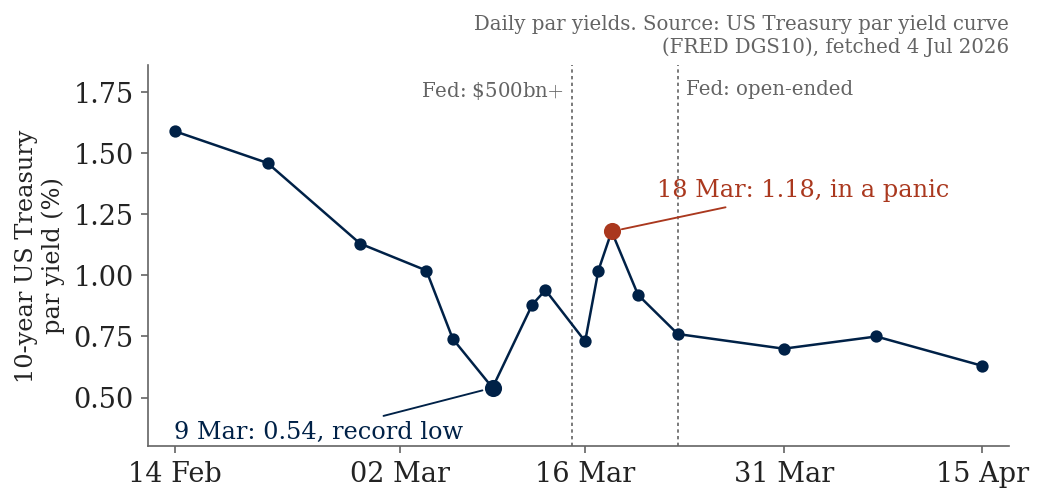

By early 2020, this crowded, highly leveraged position sat quietly in the background of the Treasury market, the deepest and supposedly safest government bond market in the world. Then Covid-19 hit. In the last days of February and first days of March, investors rushed into Treasuries as a safe haven, driving the 10-year yield down to about 0.54% on 9 March, a historic low. Within days, the crisis turned into something else: a broad dash for cash. Funds needed dollars everywhere at once, for margin calls, for redemptions, for anything that could be turned into liquidity fast. Basis trades, financed in repo and marked to market daily on the futures leg, were an obvious place to raise cash from, so funds began unwinding them, selling the cash bonds and buying back the futures.

That selling landed directly on the asset everyone had just fled into for safety. Between 9 and 18 March, the 10-year Treasury yield reversed sharply, rising from about 0.54% to about 1.18%, a move of 64 basis points in just nine days, the opposite direction from what a simple flight-to-safety story would predict. Bid-ask spreads widened, repo rates on Treasury collateral spiked, and the basis itself, normally a sleepy few basis points, blew out. The safe asset had briefly stopped acting safe.

The Fed as buyer of last resort

The Federal Reserve responded at a scale that matched the shock. On 12 and 13 March, the New York Fed sharply increased its repo operations to ease funding strains. On 15 March, the Fed cut its policy rate to 0-0.25% and pledged to buy "at least $500 billion" of Treasuries. On 23 March, it went further still and made its purchases open-ended, promising to buy Treasury and agency mortgage-backed securities "in the amounts needed to support smooth market functioning." Purchases peaked at about $75 billion a day between 19 March and 1 April, and by the end of the quarter the Fed had bought more than $1 trillion of Treasuries in total, the fastest balance-sheet expansion in its history to that point. The market stabilised. Hedge funds, for their part, had by then sold more than $200 billion of cash Treasuries and cut their total Treasury exposure by about $430 billion.

The trade survives, the rules change

The episode did not end the trade. By May 2025, leveraged funds' short Treasury-futures notional, a broad proxy across the 2-, 5- and 10-year contracts, had grown back to more than $1 trillion. What changed was regulation. In December 2023, the US Securities and Exchange Commission adopted a rule requiring central clearing for large parts of the Treasury cash and repo markets, a direct response to episodes like this one. Compliance dates, after a further extension in February 2025, run to the end of 2026 for cash Treasury transactions and mid-2027 for repo.

The case therefore turns on a single distinction. The trade never stopped being duration-neutral. It was never funding-neutral, and funding is what broke.

| Date | Event |

|---|---|

| 2017-2019 | The cash-futures basis trade grows sharply; hedge funds' total Treasury exposure rises by almost $1 trillion over this period. |

| Late Feb 2020 | Covid-19 fears spread through global markets. The 10-year Treasury yield, around 1.5-1.6% in mid-February, starts falling as investors seek safety. |

| 9 Mar 2020 | The 10-year Treasury yield falls to about 0.54%, a historic low, as the flight to safety peaks. |

| 9-13 Mar 2020 | Treasury market functioning deteriorates: spreads widen, repo rates rise, and the cash-futures basis blows out. Leveraged funds start unwinding basis positions. |

| 12-13 Mar 2020 | The New York Fed sharply increases repo operations to ease funding strains. |

| 15 Mar 2020 | The Fed cuts its policy rate to 0-0.25% and pledges to buy "at least $500 billion" of Treasuries. |

| 18 Mar 2020 | The 10-year Treasury yield reaches about 1.18%, the peak of the reversal, a 64 basis point rise from the 9 March low in nine days. |

| 19 Mar-1 Apr 2020 | The Fed's Treasury purchases reach a peak pace of about $75 billion a day, its fastest balance-sheet expansion to that point. |

| 23 Mar 2020 | The Fed makes its asset purchases open-ended, removing the earlier dollar cap. |

| 2020 Q1 | The Fed buys more than $1 trillion of Treasury securities in total, stabilising the market. |

| 13 Dec 2023 | The SEC adopts a rule mandating central clearing for large parts of the Treasury cash and repo markets. |

| May 2025 | Leveraged funds' short Treasury-futures notional, summed across the 2-, 5- and 10-year contracts, exceeds $1 trillion again. |

The mechanics, in course language

Three legs, one thin spread

The trade has three legs. Leg 1: buy the cheapest-to-deliver Treasury bond. Leg 2: sell the matching Treasury futures contract short. Leg 3: finance the bond purchase in the repo market, rolling the funding over short intervals, often overnight. Netting legs 1 and 2 together leaves not a bet on the level of interest rates, but the basis, the net cost of carry. That is coupon income earned while holding the bond, minus the financing cost of carrying it, minus or plus the futures contract's own richness or cheapness relative to fair value. The basis is normally only a few tens of basis points, and it converges towards zero as the contract approaches delivery.

Because the basis is thin, the trade is only worthwhile at high leverage. A large enough position, financed almost entirely in overnight repo against a very small sliver of investor equity, turns a few tens of basis points of basis into a double-digit annual return on that equity. This is the same leverage mechanism at work as with margin: a small move gets amplified into a large one on equity. Here, it is applied to the safest asset in the world.

Neutral on rates, exposed on funding

The structural fact that matters is that the trade is close to duration-neutral. Long the bond's duration, short the futures' duration, so the two largely cancel, which is why the position looks safe from the direction of interest rates. What it is not neutral to is funding. The bond is financed in repo that must be rolled, typically overnight, and the futures position is marked to market and margined every day. If either financing channel tightens, for example if repo rates spike or margin requirements rise in a broad market panic, the fund must find cash fast, or unwind. Unwinding means selling the cash bond and buying back the futures, in a hurry, in the same market that is already under stress. Margin turns credit risk into liquidity risk, and it does so even inside the market regarded as the ultimate safe haven.

Three building blocks, one shock

March 2020 is the proof. As Covid-19 fears spread, investors first rushed into Treasuries, pushing the 10-year yield to its low. Then, as the crisis widened into a dash for cash, funds needed dollars for margin calls and redemptions everywhere, including from their basis positions. Selling Treasuries to raise cash, and the unwind of basis-trade positions alongside it, contributed to the sharp yield reversal described above. The conversion factor and cheapest-to-deliver bond link the futures price to a specific cash bond; the basis is the net cost of carry applied to bonds instead of commodities; and margin turns funding stress into forced sales. None of these three ideas is new on its own. What March 2020 shows is what happens when all three combine at trillion-dollar scale, financed overnight, in a single market shock.

The mathematics

The question worth answering first is how much a normal basis gain and a stress-scale adverse move are worth once leverage is applied. The course's own stylised illustration uses 50-times leverage on the basis trade: a 25 basis point basis gain becomes a return on equity of 12.5%, and a 20 basis point adverse move becomes a loss of 10.0% of equity. The formula behind that is simple: leverage multiplied by the basis move, in percentage points.

$$\text{RoE} = L \times \text{basis move (bp)} \div 100$$

That stylised number is worth setting against something genuinely measured. The Office of Financial Research finds a mean leverage of about 21-to-1 for large basis traders, using actual position and equity data rather than a stylised illustration. Applying the same 25bp gain and 20bp adverse move at this measured leverage gives smaller, but still large, swings in equity:

$$\text{RoE}_{gain} = 21 \times 25 \div 100 = 5.25\%, \qquad \text{RoE}_{loss} = 21 \times 20 \div 100 = -4.2\%$$

The headline yield move for this case is worth recomputing directly rather than simply quoting it:

$$1.18\% - 0.54\% = 0.64 \text{ percentage points} = 64 \text{ basis points}$$

# (a) Stylised case: 50-times leverage

L_stylised = 50

basis_earned_bp = 25

adverse_bp = 20

roe_gain_pct = L_stylised * basis_earned_bp / 100

roe_loss_pct = L_stylised * adverse_bp / 100

print(roe_gain_pct)

print(-roe_loss_pct)

# (b) Same arithmetic using the OFR's measured leverage figure (21-to-1)

L_real = 21

roe_gain_pct_real = L_real * basis_earned_bp / 100

roe_loss_pct_real = L_real * adverse_bp / 100

print(roe_gain_pct_real)

print(-roe_loss_pct_real)

# (c) The headline yield move, recomputed rather than just quoted

y_low, y_high = 0.54, 1.18

move_bp = round((y_high - y_low) * 100, 2)

print(move_bp)Output

12.5

-10.0

5.25

-4.2

64.0Both leverage figures turn a single-digit or low-double-digit basis point move, trivial for the underlying bond, into a double-digit swing in equity. That gap between what happens to the bond and what happens to the fund's equity is the entire mechanism behind the forced selling in March 2020. The two leverage numbers differ because they are not competing estimates of the same thing. The 50-times figure is a stylised illustration; 21-to-1 is the OFR's measured mean across large basis traders, which itself carries wide dispersion across funds and over time. They are two different points in a plausible range, not a contradiction.

Data and facts

| Quantity | Value | Source |

|---|---|---|

| 10-year Treasury yield, 9 Mar 2020 (low) | ≈0.54% | US Treasury/FRED DGS10 |

| 10-year Treasury yield, 18 Mar 2020 (peak) | ≈1.18% | US Treasury/FRED DGS10 |

| Yield move, 9-18 Mar 2020 | 64bp in 9 days | Vissing-Jorgensen, NBER WP 29128 (2021) |

| Fed Treasury-purchase pledge, 15 Mar 2020 | at least $500bn | Federal Reserve, Implementation Note, 15 Mar 2020 |

| Fed peak purchase pace, 19 Mar-1 Apr 2020 | ≈$75bn/day | Federal Reserve press releases; CRS Report R46411 |

| Total Fed Treasury purchases, 2020 Q1 | >$1 trillion | Vissing-Jorgensen, NBER WP 29128 (2021) |

| Hedge funds' cash Treasuries sold in the stress | >$200bn | Barth and Kahn, OFR WP 21-01 (2021) |

| Mean leverage, large basis traders | ≈21-to-1 | OFR Brief 20-01 (2020); Barth and Kahn (2021) |

| Pure basis-trade size, Sep 2023 | $260-574bn | Glicoes et al., FEDS Notes (2024) |

| Leveraged funds' short Treasury-futures notional, May 2025 | >$1 trillion (proxy) | Chicago Fed Letter No. 516 (2026) |

| SEC Treasury clearing mandate adopted | 13 Dec 2023 | SEC final rule; Release No. 34-102487 (2025) |

A caution belongs in any discussion of this case: there is no single number for "the size of the basis trade." Leveraged funds' total short Treasury-futures notional is often quoted at more than $1 trillion, but that is a broad proxy that also captures directional shorting unrelated to the basis arbitrage. The Fed's own narrower estimate of the pure basis trade specifically puts it at $260-574 billion as of September 2023. These are two different, non-interchangeable measures, not conflicting versions of the same fact.

The lesson

- A duration-neutral trade is not a risk-free trade. Hedging away interest-rate exposure still leaves funding exposure: the need to roll repo financing and meet daily margin calls. When funding tightens, a hedge that is perfectly flat on rates can still force you to sell.

- Margin turns credit risk into liquidity risk, even in the safest market in the world. A paper position that is barely moving in value can still trigger a demand for cash that the holder cannot meet fast enough.

- Thin, priced gaps only exist because someone is paid to close them, and that payment is leverage. The basis is a few tens of basis points a year. Only very high leverage turns that into a viable business, and the same leverage that magnifies the gain magnifies the loss.

- A crowded one-way trade can turn the asset it is built on into the source of stress. Leveraged funds supply the short side that hedgers and asset managers need on the other side of their long futures positions, so a large enough unwind sells into, and can worsen, the very market the trade depends on.

- Regulators respond to fragility with market structure, not bans. The SEC's Treasury central-clearing mandate does not outlaw the basis trade; it extends central-counterparty architecture to the core of the bond market, trading lower peacetime cost for lower crisis risk.

Where it appears in the course

Think about it

- The basis trade is often described as "close to riskless" because it is duration-neutral. Explain why that description misses the risk that actually mattered in March 2020.

- If a fund earns 25 basis points of basis at 21-to-1 leverage, its return on equity is 5.25%. Why would a fund choose to run this trade at 50-to-1 instead, given that a 20bp adverse move at that leverage wipes out 10% of equity?

- The SEC's central-clearing mandate does not ban the basis trade or cap leverage directly. What kind of risk does moving these trades onto a central counterparty actually address, and what kind of risk does it leave untouched?

Sources

- Federal Reserve Bank of Chicago, "How the U.S. Treasury Futures Market and the Basis Trade Could Be Affected by the Treasury Clearing Mandate: Part 1 - A Primer," Chicago Fed Letter No. 516, January 2026. chicagofed.org

- Jonathan Glicoes, Benjamin Iorio, Phillip Monin and Lubomir Petrasek, "Quantifying Treasury Cash-Futures Basis Trades," FEDS Notes, Board of Governors of the Federal Reserve System, 8 March 2024. federalreserve.gov

- Daniel Barth and R. Jay Kahn, "Hedge Funds and the Treasury Cash-Futures Disconnect," Office of Financial Research Working Paper 21-01, April 2021 (published as "Hedge funds and the Treasury cash-futures basis trade," Journal of Monetary Economics, vol. 155, 2025). financialresearch.gov

- Office of Financial Research, "Recent Disruptions in Detail: (2) Basis Trades," OFR Brief Series 20-01, 16 July 2020. financialresearch.gov

- Andreas Schrimpf, Hyun Song Shin and Vladyslav Sushko, "Leverage and margin spirals in fixed income markets during the Covid-19 crisis," BIS Bulletin No. 2, Bank for International Settlements, 2 April 2020. bis.org

- Annette Vissing-Jorgensen, "The Treasury Market in Spring 2020 and the Response of the Federal Reserve," NBER Working Paper 29128, National Bureau of Economic Research, August 2021. nber.org

- Board of Governors of the Federal Reserve System, "Federal Reserve issues FOMC statement" (Implementation Note), 15 March 2020. federalreserve.gov

- Board of Governors of the Federal Reserve System, "Federal Reserve announces extensive new measures to support the economy," 23 March 2020. federalreserve.gov

- US Congressional Research Service, The Federal Reserve's Response to COVID-19: Policy Issues, Report R46411, 12 June 2020. congress.gov

- US Securities and Exchange Commission, final rule mandating central clearing for US Treasury securities, adopted 13 December 2023; Release No. 34-102487 (extension of compliance dates), February 2025. sec.gov

- US Treasury / Federal Reserve Bank of St Louis, FRED series DGS10 (10-Year Treasury Constant Maturity Rate). fred.stlouisfed.org