Research · Feb 1, 2026

New research on global monetary-policy spillovers

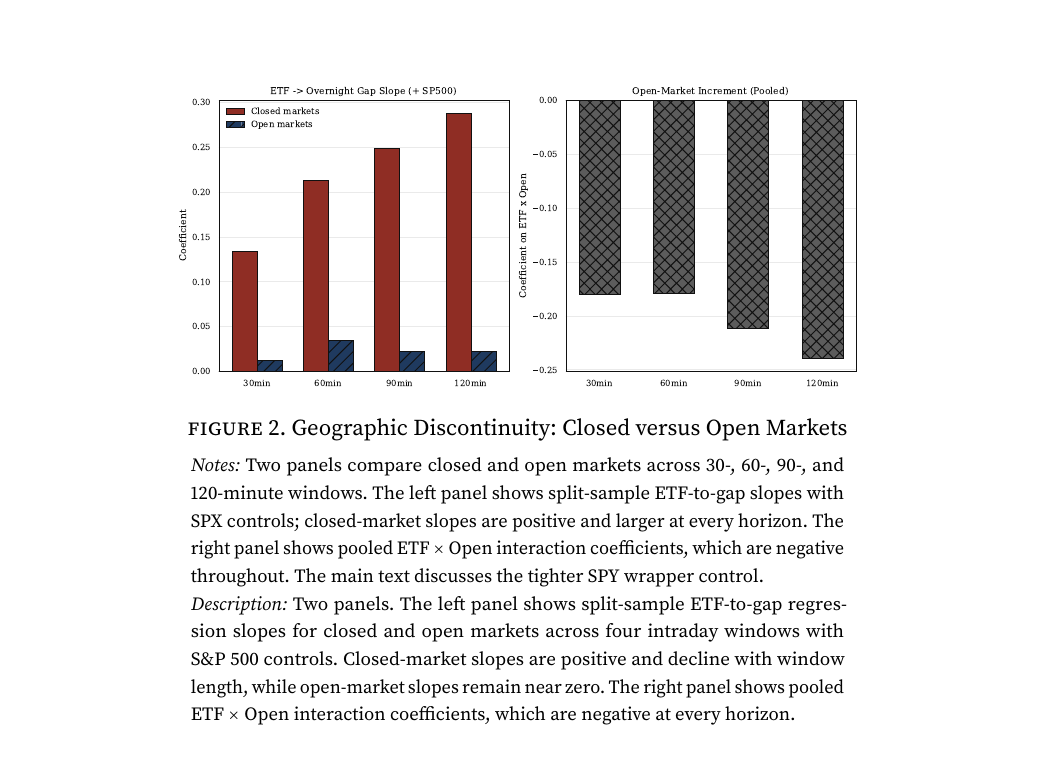

My paper, The Immediate Global Impact of US Monetary Policy, measures international spillovers in the same high-frequency window as FOMC surprises. Using US-traded country ETFs, it shows that US monetary-policy news reprices non-US equity wealth within thirty minutes, even when many foreign cash markets are closed.

Update

My research paper, The Immediate Global Impact of US Monetary Policy, is now available.

Research question

The paper asks how large immediate global equity-market spillovers from US monetary policy are when foreign markets are measured in the same high-frequency window as the FOMC surprise. The key measurement problem is that many local cash markets are closed when FOMC announcements arrive.

Main result

US-traded country ETFs reveal immediate foreign-market repricing that daily local-index designs can miss. A one-standard-deviation contractionary surprise reprices roughly $150-$300 billion in non-US equity wealth within thirty minutes, and roughly half of the response reflects local-currency equity movement rather than exchange-rate translation alone.

Read more

See the full paper page for the research design, results table and citation formats: The Immediate Global Impact of US Monetary Policy. The PDF and SSRN page are also available from the paper page.