Case studies · 2020

Bank of China's Crude Oil Treasure

A retail product tracking WTI rolled into the contract that went negative, and thousands of retail investors ended up owing the bank money.

What happened

A product built for customers who could not trade oil directly

In January 2018, Bank of China (BOC) launched a retail account product called Crude Oil Treasure (原油宝, Yuanyou Bao). Mainland Chinese customers could not trade foreign futures exchanges directly, so the product gave them a way to speculate on oil anyway: it tracked the front-month WTI or Brent futures price one-for-one, in yuan. It required 100% margin and offered no leverage, a structure that read as simple and safe: a customer posted the full notional value of the position, so on paper the most they could lose was their deposit. By April 2020, roughly 60,000 customers held positions in the product, according to Chinese media reports, though BOC itself has never published an official customer count.

The contract that went negative

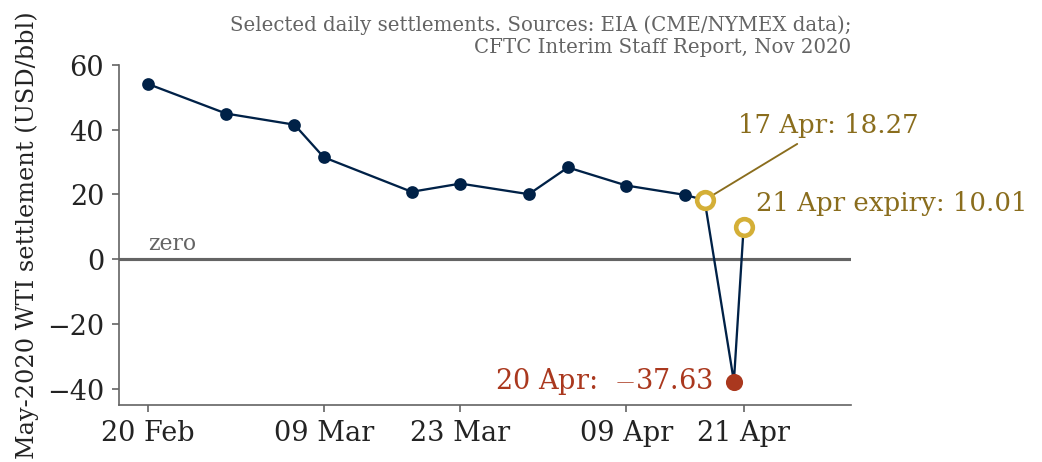

The flaw was not in the marketing. It was in the mechanics underneath it. Crude Oil Treasure tracked the front-month WTI future, and on 20 April 2020 that contract, the May-2020 WTI future, collapsed to an intraday low of about −$40.32 a barrel and settled at −$37.63 a barrel, the first-ever negative settlement in the contract's history. Cushing, Oklahoma storage was nearly full, and traders still holding the expiring contract had to pay someone to take the delivery obligation off their hands.

A roll date that turned a market event into a design failure

BOC's rival banks saw the danger coming. Industrial and Commercial Bank of China (ICBC) and China Construction Bank rolled their own equivalent paper-oil products out of the May contract on 14 April 2020, five trading days before final settlement, and so avoided the worst of the collapse. BOC scheduled its own roll for the contract's last possible trading day, 20 April 2020, the same day the contract went negative. Some or all of BOC's retail clients were still exposed when that settlement was applied.

Investors discover a debt, not just a loss

On 21 April, Chinese media and social media carried accounts of retail investors discovering they owed BOC money, not merely that they had lost their deposit: a 100%-margined, no-leverage product had produced a debt. BOC temporarily halted new positions and said it was checking the settlement data with the CME. On 22 April, it confirmed it had applied the CME's official settlement price, based on the average trade price in the contract's final two minutes, and suspended new positions altogether. Investors disputed the methodology, some arguing the bank should have used an earlier, less extreme price or closed positions before the contract's last day.

Contagion, compensation and the regulatory reckoning

Within a week, other Chinese banks, including ICBC and Shanghai Pudong Development Bank, suspended new positions in similar commodity-linked retail products covering oil, copper and soybeans, citing the same volatility risk. On 30 April, the China Banking and Insurance Regulatory Commission (CBIRC) instructed BOC to resolve the dispute lawfully and protect customers' rights. On 5-7 May, BOC offered a compensation plan: for clients with positions up to RMB 10 million, roughly covering the large majority of the 60,000 investors, the bank would absorb losses beyond the client's original deposit and refund about 20% of that deposit. Clients above that threshold, reportedly fewer than 100 people, were told they had to bear their own losses in full.

The regulatory and legal reckoning followed later that year. On 5 December 2020, CBIRC fined BOC RMB 50.5 million (about USD 7.7 million) for failures in product design, risk management, disclosure and sales, and fined four named individuals a combined RMB 1.8 million. On 31 December 2020, a Nanjing court ruled in an investor's civil suit that BOC must return 20% of the client's principal and absorb the losses beyond it. The court found that BOC had not adequately planned for a negative-price scenario, had not warned clients of that risk while trading was live, and had not liquidated positions when the margin-adequacy ratio fell below the contractual threshold. BOC's appeal was rejected on 10 February 2021, upholding the ruling.

Why the loss total moved over time

Reported loss totals differ depending on when a given piece was written. Early press in late April 2020 cited smaller estimates, some around RMB 600 million, others "over RMB 7 billion (about USD 1 billion)". The discrepancy does not reflect an error; the full scale simply was not clear yet in the first days of the crisis. The figure that stabilised once the December 2020 court case laid out the full picture, and the one this page uses throughout, is RMB 4.2 billion lost as client margin, plus a further RMB 5.8 billion owed by clients to the bank beyond their margin, for a total of about RMB 10 billion (roughly USD 1.4 billion at the prevailing exchange rate).

| Date | Event |

|---|---|

| Jan 2018 | BOC launches Crude Oil Treasure, tracking front-month WTI or Brent one-for-one, 100% margin, no leverage. |

| 14 Apr 2020 | ICBC and China Construction Bank roll their equivalent products out of the May WTI contract, five trading days before expiry. |

| 20 Apr 2020 | BOC's own scheduled roll date. May WTI settles at −$37.63/bbl (intraday low −$40.32); BOC clients still exposed. |

| 21 Apr 2020 | Retail investors report owing BOC money. BOC halts new positions and checks settlement data with the CME. |

| 22 Apr 2020 | BOC confirms it applied the CME's official settlement price; suspends new positions in the product. |

| 27-28 Apr 2020 | ICBC and Shanghai Pudong Development Bank suspend similar commodity-linked retail products. |

| 30 Apr 2020 | CBIRC instructs BOC to resolve the dispute lawfully and protect customers' rights. |

| 5-7 May 2020 | BOC offers compensation: absorb losses beyond deposit plus refund 20% of deposit, for positions up to RMB 10 million. |

| 5 Dec 2020 | CBIRC fines BOC RMB 50.5 million and four individuals a combined RMB 1.8 million. |

| 31 Dec 2020 | Nanjing court rules BOC must return 20% of principal and absorb losses beyond it; appeal rejected 10 Feb 2021. |

The mechanics, in course language

A bank account dressed as a futures position

What Crude Oil Treasure actually was matters for everything that follows. It was not itself a futures contract. It was a retail bank account product that tracked the front-month WTI or Brent futures price one-for-one, in RMB, with 100% margin and no leverage. A client who bought "long" Crude Oil Treasure was economically equivalent to holding a long position in the front-month WTI future, financed entirely by their own deposit rather than by margin borrowing.

Delivery and roll mechanics near expiry

The course concept this breaks is delivery and roll mechanics near expiry, the same lesson the negative-oil case and the May-2020 WTI settlement itself illustrate. A futures price is not simply the price of oil. It also prices the obligation to take delivery, or find someone who will, at a specific place and time. As storage at Cushing, Oklahoma filled up in April 2020, holding the expiring contract into its last trading day became dangerous, because a long holder who could not take delivery had to find a buyer willing to accept that delivery problem, at any price, including a negative one.

The roll date as a bank's design choice, not a law of nature

BOC's product added a second, non-market layer on top of this mechanical risk: an operational choice about when to roll client positions out of the expiring contract. Two rival Chinese banks rolled their equivalent products five trading days before expiry and so avoided the worst of the collapse. BOC scheduled its roll for the contract's final trading day, the same day the contract happened to settle at −$37.63. The structural fact that matters is this: a product that mechanically tracks an exchange-traded future can still embed a bank-specific design decision, in this case the roll date, that decides whether the client is exposed to a known industry-wide risk at all.

Margin without leverage is not margin without risk

This also connects to margin and leverage. Because the product used 100% margin and no leverage, BOC's clients could not simply be stopped out before the contract went negative, in the way a margined, marked-to-market futures account might trigger a forced close near zero. Once the settlement price went negative, a client with 100% margin and no borrowed leverage could nonetheless owe money beyond their deposit, because the underlying instrument itself, the future, has no floor at zero. Margin without leverage still means unlimited downside if the reference price itself can go below zero.

The mathematics

The question this section answers is how far a fully margined, no-leverage position could fall once the settlement price itself turned negative. Press reporting describes investors adding to long positions during the WTI dip toward the $20-a-barrel level shortly before expiry. A stylised long position of 1,000 notional barrels bought at $20.00/bbl, fully margined at 100%, matches Crude Oil Treasure's actual product terms and fixes the scale of the problem. This is an illustrative example, not a reported individual position.

$$P_0 = \$20.00/\text{bbl}, \qquad S_T = -\$37.63/\text{bbl}$$

$$\text{Margin posted} = P_0 \times 1{,}000 = \$20{,}000$$

$$\text{Payoff per barrel} = S_T - P_0 = -37.63 - 20.00 = -\$57.63$$

$$\text{Total payoff} = -57.63 \times 1{,}000 = -\$57{,}630$$

P0 = 20.00 # entry price, USD/bbl

S_T = -37.63 # May-2020 WTI settlement, USD/bbl

barrels = 1000

margin_posted = P0 * barrels

payoff_per_barrel = S_T - P0

total_payoff = payoff_per_barrel * barrels

owed_beyond_margin = abs(total_payoff) - margin_posted

loss_multiple = abs(total_payoff) / margin_postedOutput

margin_posted = 20000.0

payoff_per_barrel = -57.63

total_payoff = -57630.0

owed_beyond_margin = 37630.0

loss_multiple = 2.88This client loses the full $20,000 margin deposit and, because the underlying settlement price is negative, additionally owes $37,630 beyond that deposit: a total loss of 2.88 times the original margin posted. The same pattern holds at the level of one stylised client and at the level of the whole book: BOC's reported aggregate figures split RMB 4.2 billion lost as margin (42% of the reported RMB 10 billion total) against a further RMB 5.8 billion owed beyond margin (58%). That exact ratio will not hold for any given real client, since it depends on their entry price. The closer the entry price was to zero, the larger the share of the loss that falls into the "owed beyond margin" category once the settlement price turns negative.

Data and facts

| Quantity | Value | Source |

|---|---|---|

| May-2020 WTI official settlement, 20 Apr | −$37.63/bbl | CFTC Interim Staff Report, Nov 2020 |

| Intraday low, 20 Apr | −$40.32/bbl | CFTC Interim Staff Report |

| June-2020 WTI settlement, 20 Apr | +$20.43/bbl | CFTC Interim Staff Report, matches lecture5.tex |

| May-June spread, 20 Apr | $58.06/bbl | CFTC Interim Staff Report, p.12 |

| Product launch | January 2018 | CGTN, 5 Dec 2020 |

| Customers holding positions, by Apr 2020 | ≈60,000 (press-reported, not BOC-confirmed) | Caixin/Yicai Global reporting |

| Rival banks' roll, before expiry | 5 trading days (14 Apr 2020) | Structured Retail Products |

| BOC's own roll/settlement date | Contract's last trading day (20 Apr 2020) | Multiple press accounts |

| Reported aggregate loss: margin lost | RMB 4.2 billion | Yicai Global, 31 Dec 2020 court coverage |

| Reported aggregate loss: owed beyond margin | RMB 5.8 billion | Yicai Global, 31 Dec 2020 court coverage |

| Total reported loss | ≈RMB 10 billion (≈USD 1.4bn) | Yicai Global; earlier press cited smaller estimates (RMB 600m-7bn) before the full scale became clear |

| CBIRC fine, BOC and branches | RMB 50.5 million (≈USD 7.7m) | CGTN, 5 Dec 2020 |

| CBIRC fines, four named individuals | RMB 1.8 million combined | CGTN, 5 Dec 2020 |

| Nanjing court ruling | BOC returns 20% of principal, absorbs losses beyond it | Yicai Global, 31 Dec 2020; upheld on appeal 10 Feb 2021 |

The lesson

- A product that mechanically tracks a futures price does not remove the futures contract's own risks. Crude Oil Treasure was marketed as a simplified, no-leverage way to speculate on oil, but it inherited the WTI contract's delivery-driven price mechanics in full, including the possibility of a negative settlement.

- Complexity is a decision, not a law of nature. The roll date on a tracker product is a design choice made by whoever built it. BOC chose to roll on the contract's last possible day; two rival banks chose to roll five days earlier and avoided the worst of the collapse.

- Margin without leverage does not mean margin without risk. A 100%-margined position still has unlimited downside if the underlying reference price itself has no floor at zero, as the May-2020 WTI settlement demonstrated.

- Products built for retail customers who cannot access the underlying market directly concentrate operational risk inside the intermediary. When the roll-date decision turned out badly, it was BOC's own clients, not a professional trading desk, who bore the loss first.

- When a designed product fails, the resulting allocation of loss is negotiated and litigated after the fact, a regulatory fine, a partial compensation offer, a court judgement, rather than settled purely by the contract's original terms.

Where it appears in the course

Think about it

- Two rival banks rolled their equivalent products five trading days before expiry and avoided the worst of the collapse. What would it have cost BOC, in normal market conditions, to do the same, and why might a bank choose the last possible day instead?

- The product was marketed as "100% margin, no leverage", language that usually signals safety to a retail customer. What does this case suggest about the limits of that language when the underlying reference price has no floor at zero?

- BOC's compensation plan treated clients above RMB 10 million in position size differently from those below it. What might justify drawing that line, and what problems could it create?

Sources

- U.S. Commodity Futures Trading Commission, Interim Staff Report on Trading in the NYMEX WTI Crude Oil Futures Contract Leading up to, on, and around April 20, 2020, 23 November 2020. cftc.gov

- CGTN, "Bank of China fined for violating regulations on 'crude oil treasure' product," 5 December 2020. news.cgtn.com

- CGTN, "Bank of China suspends new open positions for oil trading product," 22 April 2020. news.cgtn.com

- Yicai Global, "Bank of China Must Bear Bulk of Losses From Its Oil Treasure Futures Fiasco, Court Says," reporting the 31 December 2020 Nanjing court ruling and its 10 February 2021 appeal outcome. yicaiglobal.com

- Caixin Global, "Bank of China Fined $7.7 Million After Crude Futures Carnage," 5 December 2020. caixinglobal.com

- China Banking News, "Bank of China Offers 20% Compensation Plan to Clients Burnt by Crude Oil Futures," 7 May 2020. chinabankingnews.com

- Caixin Global, "ICBC Joins Banks Suspending Risky Bets on Commodities After Oil Price Crash," 28 April 2020. caixinglobal.com

- Caixin Global, "Update: Investors in BoC's Crude Product Rage at Huge Loss Amid Oil Price Turmoil," 22 April 2020. caixinglobal.com

- South China Morning Post, "Bank of China's US$1 billion hole from plunging oil shows how investors and banks alike are ill-prepared for risks of chasing after high returns," 27 April 2020 (early estimate, superseded by later court and regulator figures). scmp.com

- Structured Retail Products, "Chinese investors turn to BoC in 'oil treasure' fiasco." structuredretailproducts.com