Case studies · 2020

Negative WTI and floating storage

Storage at the delivery point ran out of room, and traders holding expiring oil futures paid buyers to take the contracts off their hands.

What happened

A price falls through zero

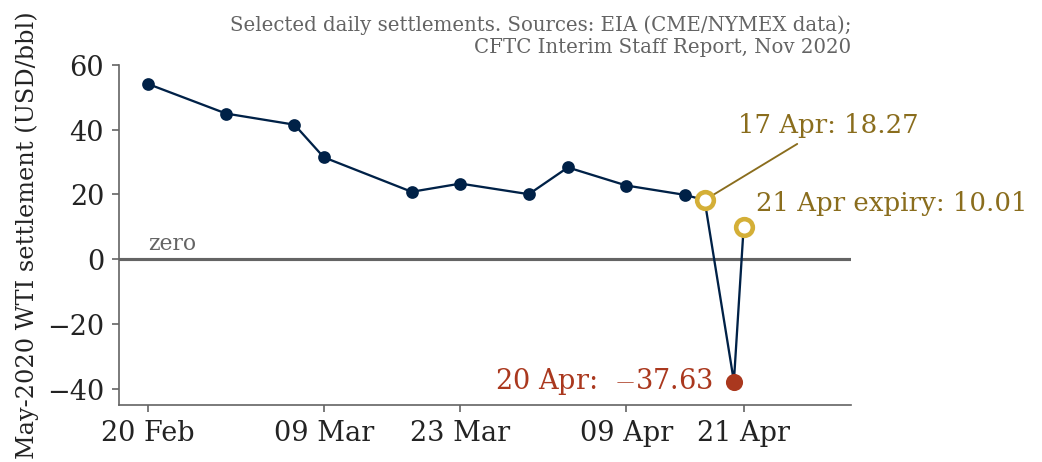

On Monday 20 April 2020, the May-2020 West Texas Intermediate (WTI) crude oil futures contract on the New York Mercantile Exchange (NYMEX) opened at $17.73 a barrel, an unremarkable price for a rough year. By early afternoon it had turned negative, and it kept falling. It touched an intraday low of −$40.32 at 2:29pm New York time, then closed, officially, at −$37.63 a barrel. That was the first time in the contract's 37-year history that the price had gone below zero. Sellers were, in effect, paying buyers to take barrels of oil off their hands.

A contract with nowhere to go

The contract expired the next day, and whoever held it at expiry owed physical delivery of 1,000 barrels of crude at Cushing, Oklahoma, the pipeline hub that is the contract's sole delivery point. Normally that is not a problem: almost every trader closes out or rolls into the next month long before expiry, and only a small number of contracts stand for delivery. April 2020 was not normal. Covid-19 lockdowns had gutted demand for petrol and jet fuel just as a Saudi-Russian price war added extra barrels to the market. Cushing's storage tanks, which can hold around 76 million barrels, were reported at about 76% full by the Friday before the crash, and most of the remaining space was already leased or promised to someone else.

The only way out was to pay someone to take it

That left a small number of traders still holding the May contract in an impossible position. They could not take delivery, because there was nowhere to put the oil. They could not simply let the contract lapse either, because a futures contract is a binding obligation, not an option. Their only way out was to sell, at whatever price a buyer with spare storage would accept. Whoever could supply that storage, for instance by chartering an oil tanker to hold crude at sea rather than move it, was, in effect, being paid to solve someone else's problem. The very next day, the June contract, now the front month, traded at a completely ordinary +$20.43. The gap between the two, $58.06 a barrel, was the price the market put on one month of storage space.

Storage, not the barrel, was the scarce asset

The shipping data tell the same story. Floating storage on tankers hit record levels within a week: about 60 very large crude carriers, each able to hold roughly 2 million barrels, were chartered to sit at sea and wait. The May contract itself expired the following day at +$10.01, a perfectly normal price, once the traders who had nowhere to put physical oil were gone from the market.

| Date | Event |

|---|---|

| 6 Mar 2020 | OPEC+ fails to agree a production cut; Saudi Arabia raises output, starting a price war on an already oversupplied market. |

| 30 Mar 2020 | May WTI settles at $20.09/bbl, an 18-year low close at the time. |

| 12 Apr 2020 | OPEC+ agrees a record 9.7 million barrel-a-day cut, but it starts 1 May, too late to help the expiring May contract. |

| 17 Apr 2020 | May WTI closes at $18.27/bbl. Cushing storage is reported at about 76% of working capacity. |

| 20 Apr 2020 | May WTI falls below zero at 2:08pm ET, hits an intraday low of −$40.32, and settles at −$37.63. June settles at +$20.43 the same day. |

| 21 Apr 2020 | The May contract expires, settling at +$10.01 as June becomes the front month. |

| 23 Nov 2020 | The US Commodity Futures Trading Commission publishes its Interim Staff Report on the episode, the primary source for this page. |

Background

WTI is the US benchmark crude grade, priced and delivered at Cushing, Oklahoma, a pipeline and storage hub. Unlike a financial future on a stock index, the NYMEX WTI contract is physically deliverable: a trader still holding the contract at expiry must make or take delivery of 1,000 barrels a lot. That is the detail that drives everything else in this case. Most participants, hedgers and speculators alike, close their position or roll it into a later month long before that point, precisely to avoid the delivery obligation. In April 2020, Covid-19 travel and lockdown restrictions had collapsed demand for road and air fuel just as Cushing's tanks were filling from the Saudi-Russia price war. With storage scarce and the contract about to expire, the small remaining pool of long positions had far fewer ways out than usual, and far less room to manoeuvre.

The mechanics, in course language

Crude oil is a consumption asset, not an investment asset, and that distinction does all the work in this case. For an investment asset, both sides of the no-arbitrage argument work, and together they pin the forward price down to an equation: \(F_0 = S_0 e^{rT}\) (extended for income, dividend yield, or storage costs). For a consumption asset, only one side survives. If the future trades too high, anyone holding physical inventory can buy spot, store it, and sell the future, and that trade caps the price. The mirror trade would require selling spot inventory short and buying it back later, but refiners who hold physical oil will not do this, because it means halting production, and they value having the barrel on hand, a value known as the convenience yield. That asymmetry leaves an inequality, not an equation:

$$F_0 \le S_0\, e^{(r+u)T}$$

April 2020 is what happens when even the ceiling-side trade stops working. That ceiling assumes a trader can always buy spot, store it, and sell the future. By 17 April, Cushing was reported at about 76% of working capacity, with the rest largely spoken for. A trader who did not want, or could not arrange, storage had no way to convert the expiring contract into a stored barrel. The only way out was to sell the contract outright, to anyone who could supply the missing storage. Once that arm of the arbitrage was gone, nothing capped the price any more, not even zero.

The mathematics

One number fixes the scale of the mismatch on 20 April 2020: the May–June spread of $58.06 a barrel, which is the market's one-day price for a month of storage.

$$\text{Spread} = F_{June} - F_{May} = 20.43 - (-37.63) = 58.06 \text{ USD/bbl}$$

On one NYMEX contract, which is 1,000 barrels, that spread is worth:

$$58.06 \times 1{,}000 = \$58{,}060 \text{ per contract}$$

may_settle_20apr = -37.63 # USD/bbl, official May-2020 WTI settlement

june_settle_20apr = 20.43 # USD/bbl, official June-2020 WTI settlement

contract_size = 1000 # barrels per NYMEX WTI futures contract

spread = june_settle_20apr - may_settle_20apr

spread_per_contract = spread * contract_sizeOutput

spread = 58.06 USD/bbl

spread_per_contract = $58,060.00This number is a per-contract illustration of the spread, not a claim about what any specific trader actually made. The CFTC's own report does not identify or evaluate any individual trader's activity, so the $58,060 figure stands as a teaching illustration of the storage price, not a real-world profit-and-loss statement.

Data and facts

| Quantity | Value | Source |

|---|---|---|

| May-2020 WTI official settlement, 20 Apr | −$37.63/bbl | CFTC Interim Staff Report, Nov 2020 |

| Intraday low, 20 Apr, 2:29pm ET | −$40.32/bbl | CFTC Interim Staff Report |

| June-2020 WTI settlement, 20 Apr | +$20.43/bbl | Congressional Research Service, IN11354 |

| May-June spread, 20 Apr | $58.06/bbl | CFTC Interim Staff Report, p.24 |

| Cushing, OK working storage capacity | ≈76 million bbl | EIA, cited in CFTC report, p.13 |

| Cushing utilisation, 17 Apr 2020 | ≈76% of capacity | CFTC Interim Staff Report, Fig. 3 |

| May contract open interest, start of Apr → 20 Apr session | 634,727 → 108,593 (−83%) | CFTC Interim Staff Report, pp.15-16 |

| VLCC tankers chartered for floating storage, late Apr | ≈60 (up from <10 in Feb) | Reuters shipping-source reporting, Apr 2020 |

The lesson

- A futures price is a claim about a specific contract, not about the commodity in general. The May-2020 contract went negative because of its delivery terms, physical, Cushing-only, expiring imminently, at a moment storage ran out. It did not mean crude oil itself had negative value.

- A no-arbitrage bound is only as strong as its weakest precondition. The ceiling on a consumption asset's price assumes someone can always buy spot, store it, and sell the future. When storage itself became unavailable, the ceiling did not bend, it became meaningless.

- Roll and offset dates matter as much as the direction of the trade. Most market participants never intend to take delivery, and the traders caught by the negative print were disproportionately those still holding the expiring contract close to its last trading day.

- Where one arm of an arbitrage cannot operate, whoever can supply the missing piece is paid a scarcity price. The $58.06 spread was, in effect, the market's one-day price for a month of storage, which is exactly why floating storage and tanker charters spiked in the same week.

Where it appears in the course

Think about it

- If you had been long the May contract on the morning of 20 April 2020, what were your realistic ways out, and why did each one narrow as the day went on?

- Floating storage on tankers is expensive: fuel, crew and insurance all cost money. Why would anyone charter a VLCC just to hold oil rather than move it?

- The June contract traded at a perfectly ordinary +$20.43 the same day the May contract went to −$37.63. What does that tell you about whether the "oil market" as a whole had a single price that day?

Sources

- US Commodity Futures Trading Commission, Interim Staff Report: Trading in NYMEX WTI Crude Oil Futures Contract Leading up to, on, and around April 20, 2020, 23 November 2020. cftc.gov

- US Commodity Futures Trading Commission, "CFTC Staff Publishes Interim Report on NYMEX WTI Crude Contract Trading," press release, 23 November 2020. cftc.gov

- Congressional Research Service, Michael Ratner and Heather L. Greenley, Crude Oil Futures Prices Turn Negative, CRS Insight IN11354, 22 April 2020. congress.gov

- US Energy Information Administration, "WTI crude oil futures prices fell below zero because of low liquidity and limited available storage," Today in Energy, April 2020. eia.gov

- US Energy Information Administration, weekly and daily petroleum data series (NYMEX front-month settlements; Cushing, OK ending stocks). eia.gov

- Reuters (Laila Kearney and Devika Krishna Kumar), "No Vacancy: Main U.S. oil storage in Cushing is all booked," 21 April 2020.

- MarketWatch (Myra P. Saefong), "The oil market is running out of storage space and production cuts loom," 21 April 2020.