Case studies · 2022

The UK LDI gilt crisis

Pension funds used leveraged interest-rate hedges that were working exactly as designed, until a budget shock triggered a collateral spiral that forced the central bank to step in.

What happened

The mini-budget

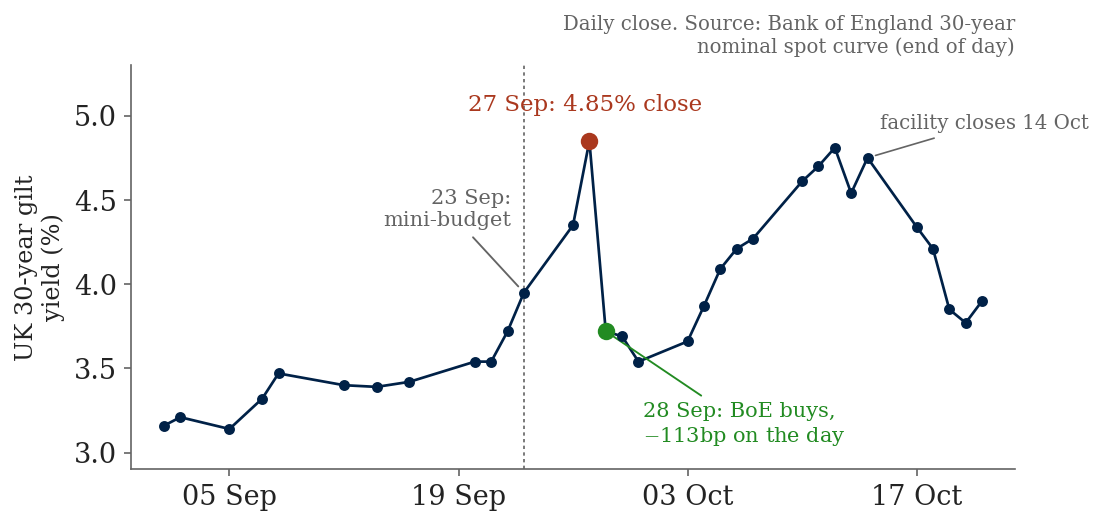

On 23 September 2022, the UK's new Chancellor, Kwasi Kwarteng, delivered "The Growth Plan," a fiscal statement quickly nicknamed the "mini-budget." It announced about GBP 45 billion a year of unfunded tax cuts, with no accompanying forecast from the Office for Budget Responsibility. The Institute for Fiscal Studies called it the largest package of tax cuts since 1972. Investors read the statement as a loss of fiscal discipline and sold UK government bonds, known as gilts, hard.

Yields break

The 30-year gilt yield closed at 3.95% on the day of the mini-budget. Over the following days it kept rising, reaching a peak closing level of 4.85% on 27 September, and moving higher still intraday on 28 September, when the Bank of England's Deputy Governor Jon Cunliffe later told the Treasury Select Committee that the 30-year yield had touched above 5% and moved through a 127 basis point range within a single day. Cunliffe's own headline figure, given in a letter to the Committee on 5 October 2022, was that the 30-year yield "rose by 160 basis points in just a few days," a move he described as "more than twice as large as the largest move since 2000." This page works with a closer reading of that same letter: roughly 1.2 percentage points over three trading days.

The speed of that move mattered more than its size. UK defined-benefit pension schemes run liability-driven investment (LDI) strategies: they hedge the risk of falling interest rates using long-dated gilts and receive-fixed interest-rate swaps, often financed with leverage of roughly two to four times, with a median of about 2.5 times at the September 2022 peak. When yields rose sharply, the mark-to-market value of those hedge positions fell, and swap counterparties and gilt repo lenders demanded variation margin and additional collateral in cash, immediately. Bank of England analysis put the cumulative collateral and margin calls on LDI funds between 23 and 28 September at about GBP 66 billion.

The doom loop

Funds that could not post cash fast enough had only one lever left: sell gilts to raise it. Every LDI fund faced the same problem at the same time, so the forced selling itself pushed gilt prices down and yields up further, generating the next round of margin calls. Market participants named this self-reinforcing spiral the "doom loop," and it threatened to become disorderly enough to damage the wider gilt market and, with it, financial stability.

The Bank of England steps in

On 28 September 2022, the Bank of England's Financial Policy Committee recommended intervention. The Bank announced temporary purchases of long-dated conventional gilts, initially up to GBP 5 billion per auction across 13 auctions, an announced capacity of up to GBP 65 billion. The 30-year yield fell back to a close of 3.72% that same day, a 113 basis point one-day drop, the largest one-day fall of the whole episode. On 10 and 11 October, the Bank raised the per-auction cap to GBP 10 billion and added index-linked gilts to the purchases, reflecting their weight in LDI funds' repo collateral. The operation closed as scheduled on 14 October 2022. Total purchases came to about GBP 19.3 billion, split between GBP 12.1 billion of conventional gilts and GBP 7.2 billion of index-linked gilts, well under a third of the announced capacity.

Political fallout, and the funding ratio that never broke

The political fallout followed fast. Kwasi Kwarteng was dismissed as Chancellor on 14 October, the same day the Bank's operation closed. Prime Minister Liz Truss resigned on 20 October, after just 44 days in office, the shortest tenure of any UK prime minister. The Bank unwound its gilt purchases in an orderly, demand-led fashion between late November 2022 and 12 January 2023, fully dispensing of the portfolio by 12 January 2023.

What is easy to miss in this sequence is that the pension schemes themselves were, on aggregate, becoming better funded throughout the crisis, not worse. Because pension liabilities have far longer duration than the assets typically used to hedge them, a rise in interest rates cuts the present value of the liabilities by more than it cuts the value of the hedge assets. Bank of England data presented by Executive Director Sarah Breeden in November 2022 showed aggregate defined-benefit liabilities in the Pension Protection Fund's PPF 7800 index falling by 36%, from about GBP 1,689 billion to about GBP 1,076 billion, between end-2021 and end-September 2022, while assets fell by only 20%, from about GBP 1,818 billion to about GBP 1,451 billion. Net assets across the index were, in Breeden's words, "nearly three times higher." By end-December 2022, the PPF 7800 funding ratio stood at 136.5%. The hedge was doing exactly its job on solvency. What nearly broke the system was the mismatch between how fast collateral is called and how slowly a correct hedge shows up in the funding numbers.

| Date | Event |

|---|---|

| 22 Sep 2022 | Bank of England raises Bank Rate by 50bp to 2.25% and confirms gilt sales under quantitative tightening from October. The market absorbs this smoothly, with about a 20bp move in gilt yields on the day. |

| 23 Sep 2022 | Chancellor Kwasi Kwarteng delivers the mini-budget, about GBP 45bn a year of unfunded tax cuts with no OBR forecast. The 30-year gilt yield closes at 3.95%. |

| 23-28 Sep 2022 | Thirty-year gilt yields keep rising; Cunliffe later describes a 160bp move "in just a few days." LDI funds face cumulative collateral and margin calls of about GBP 66bn. |

| 27 Sep 2022 | 30-year gilt yield closes at 4.85%, the peak daily close of the episode. |

| 28 Sep 2022 | Intraday, the 30-year yield rises above 5%, a 127bp intraday range. The Bank of England announces gilt purchases of up to GBP 65bn capacity. The 30-year close falls to 3.72%, a 113bp one-day drop. |

| 10-11 Oct 2022 | The Bank raises the per-auction cap to GBP 10bn and adds index-linked gilts to the purchases. |

| 14 Oct 2022 | Gilt purchase operations close as scheduled. Total purchases: about GBP 19.3bn (GBP 12.1bn conventional, GBP 7.2bn index-linked). Kwasi Kwarteng is dismissed as Chancellor. |

| 20 Oct 2022 | Prime Minister Liz Truss resigns after 44 days in office, the shortest tenure of any UK prime minister. |

| 29 Nov 2022 - 12 Jan 2023 | The Bank unwinds its financial-stability gilt purchases in an orderly, demand-led fashion, fully dispensing of the portfolio by 12 January 2023. |

The mechanics, in course language

This case sits on the swap thread built across Lectures 4, 6 and 7. It is not a story about a bad bet. It is a story about a hedge that was working, and about the difference between being right on value and having the cash to prove it.

Matching duration to a distant liability

Defined-benefit pension schemes owe payments decades into the future. When long-term interest rates fall, the present value of those promised payments rises, since the same future cash flows are now discounted at a lower rate. This is the duration logic from Lecture 4: a fixed set of future payments is worth more when the discount rate drops, and worth less when it rises. To protect themselves against falling rates increasing their liabilities, UK pension schemes hold liability-driven investment mandates: portfolios of long-dated gilts and receive-fixed interest-rate swaps, chosen so the assets move in the same direction as the liabilities when rates move. This is the textbook hedge: match the duration of the assets to the duration of the liabilities.

Small capital, large notional

The leverage came from wanting the same hedge for less capital. Rather than buy enough long gilts outright to match a scheme's full liability duration, LDI funds used gilt repo and receive-fixed swaps to get more exposure to long-dated interest rates per pound of capital, typically two to four times, with a median around 2.5 times at the September 2022 peak. This "small capital, large notional" feature runs through every levered derivative position in the course, from futures margin in Lecture 6, to the basis trade, to a swap's notional versus the cash actually posted in Lecture 7.

The margin call that leverage magnified

When the mini-budget hit, long-dated gilt yields spiked. A rise in yields cuts the value of a long-dated bond or a receive-fixed swap, so the fund's assets fell in mark-to-market value. Because the funds were levered, this loss was large relative to their capital, even though it was a genuinely small move relative to the notional being hedged. Swap counterparties and gilt repo lenders demanded variation margin and additional collateral, in cash, immediately, the same margining mechanic seen with futures in Lecture 6. A fund that could not post that cash fast enough had to sell gilts to raise it. Selling gilts into a market where every other LDI fund was trying to do the same thing pushed gilt prices down further and yields up further, which then generated the next round of margin calls. That is the "doom loop": rising yields force gilt sales, gilt sales push yields higher, and the cycle repeats until something interrupts it.

Right on solvency, exposed on liquidity

The point worth holding is that, over the same period, the schemes' overall funded position was improving, not deteriorating. Because liabilities are far longer-duration than the assets backing them, a rise in rates cuts the present value of the liabilities by more than it cuts the value of the assets. The hedge was winning. What nearly broke the system was liquidity, not solvency: margin calls demand cash on a timetable measured in days, while the gain on a correctly working hedge only shows up as an improved funding ratio over a much longer horizon. This is the same lesson drawn from Metallgesellschaft and from the Treasury basis trade: a position can be right on value and still fail for want of cash.

A backstop that worked by being credible

The Bank of England's intervention was deliberately narrow and temporary: buy long-dated gilts to stop the forced-selling spiral, give funds time to raise cash and deleverage in an orderly way, and then unwind the purchases once the spiral stopped, all without changing the stance of monetary policy, since the Bank was simultaneously raising rates to fight inflation. That the Bank only needed to use about 30% of its announced GBP 65 billion capacity is itself informative: announcing a large, credible backstop reduced the urgency of the fire sale, so the facility did not need to be fully drawn to do its job.

The mathematics

Two calculations fix the scale of what happened. The first uses only real, sourced figures and shows how small the Bank's actual footprint was relative to the cash the crisis generated. The second is a stylised, illustrative sketch of why a leverage ratio of about 2.5 times can turn a survivable yield move into an urgent cash call.

Part A: scale of the Bank of England's intervention (real, sourced numbers).

$$\text{Share of announced capacity used} = \frac{19.3}{65.0} = 29.7\%$$

$$\text{Ratio of margin calls to the Bank's purchases} = \frac{66.0}{19.3} = 3.42\times$$

These two ratios show that the Bank's purchases were far smaller than the total cash demand the crisis generated. Most of the GBP 66 billion was met by funds selling non-gilt assets, drawing down cash buffers, and pension schemes injecting fresh capital into their LDI mandates, not by the Bank of England buying gilts. The Bank's role was to stop the self-reinforcing price spiral in the gilt market itself, not to fund the whole margin call.

Part B: stylised leverage arithmetic (illustrative only, not a real fund's disclosed figures). Treat the scheme capital, leverage multiple and duration proxy below as illustrative numbers chosen to make the mechanism clear; only the 1.2 percentage point yield move is the course's own sourced figure.

$$\text{Notional} = \text{Capital} \times \text{Leverage} = 100 \times 2.5 = 250 \text{ (GBP m)}$$

$$\text{Price fall} = \text{Modified duration} \times \Delta y = 20 \times 0.012 = 24\%$$

$$\text{Loss} = \text{Notional} \times \text{Price fall} = 250 \times 0.24 = \text{GBP } 60\text{m}$$

$$\text{Loss as share of capital} = \frac{60}{100} = 60\%$$

# Stylised, for illustration only. Capital, leverage, and duration are illustrative;

# the yield move (1.2pp) is the course's own sourced figure (Cunliffe letter, 5 Oct 2022).

capital = 100 # GBP m of scheme capital placed in the LDI mandate

leverage = 2.5 # median LDI leverage at the Sept-2022 peak

notional = capital * leverage

delta_yield = 0.012 # 1.2 percentage points, the course's headline three-day move

mod_duration = 20 # years, illustrative order-of-magnitude for a long gilt/swap book

price_fall_pct = mod_duration * delta_yield

loss = notional * price_fall_pct

loss_as_pct_of_capital = loss / capital * 100Output

notional = 250.0 # GBP m of long gilt / receive-fixed swap exposure

price_fall_pct = 0.24 # 24% fall in the mark-to-market value of the hedge book

loss = 60.0 # GBP m

loss_as_pct_of_capital = 60.0These illustrative inputs show that a 1.2 percentage point yield rise generates a mark-to-market move against the hedge book equal to about 60% of the scheme's capital in the mandate, arriving as a margin or collateral call within days, even while the pension scheme's overall funding ratio is improving over the same period. That is the arithmetic behind the case's key line: margining can turn a winning hedge into a scramble for cash.

Data and facts

| Quantity | Value | Source |

|---|---|---|

| Mini-budget size, 23 Sep 2022 | ≈GBP 45bn/yr unfunded tax cuts | IFS, 23 Sep 2022 |

| 30-year gilt yield, close, 23 Sep 2022 | 3.95% | Bank of England fitted spot curve |

| 30-year gilt yield, close, 27 Sep 2022 (peak close) | 4.85% | Bank of England fitted spot curve |

| 30-year gilt yield, intraday, 28 Sep 2022 | above 5%, 127bp intraday range | Cunliffe letter, 5 Oct 2022 |

| 30-year gilt yield, close, 28 Sep 2022 | 3.72% (−113bp on the day) | Bank of England fitted spot curve |

| Cumulative LDI collateral/margin calls, 23-28 Sep | ≈GBP 66bn | Wilkins (2024), citing BoE analysis |

| BoE gilt purchases, announced capacity | up to GBP 65bn | BoE Market Notice, 28 Sep 2022 |

| BoE gilt purchases, actual total | ≈GBP 19.3bn (12.1 conventional + 7.2 index-linked) | BoE Quarterly Bulletin, 2023 |

| LDI fund leverage, median at Sep 2022 peak | ≈2.5× (range 2×-4×) | Central Bank of Ireland FS Note, 2023 |

| PPF 7800 liabilities, end-2021 → end-Sep 2022 | −36% (≈GBP 1,689bn → ≈1,076bn) | Breeden speech, 7 Nov 2022 |

| PPF 7800 assets, end-2021 → end-Sep 2022 | −20% (≈GBP 1,818bn → ≈1,451bn) | Breeden speech, 7 Nov 2022 |

| PPF 7800 funding ratio, end-Dec 2022 | 136.5% | PPF 7800 Index |

The lesson

- Margin turns credit risk into liquidity risk. A hedge can be correct in present-value terms and still force a fund to find cash within days, because collateral calls are settled now, while the benefit of a correct hedge only shows up as an improved funding ratio over years.

- Leverage does not change whether a position is right, only how fast being right can bankrupt you if you cannot fund the interim cash calls. The LDI funds were solvent throughout; the leverage in front of that solvency is what made the timing lethal.

- A hedge designed against the risk you expect (falling rates hurting liability values) can still generate a severe cash crisis from the opposite move (rising rates), because the cash mechanics of margin do not care which direction "helped" the fund's true economic position.

- Concentrated, correlated positioning turns an isolated shock into a market-wide one. LDI funds were the natural buyers of long-dated and index-linked gilts, so when they all needed to sell at once, there was no offsetting buyer to absorb the flow, and the price impact fed back into the very yields that triggered the selling.

- A central bank backstop can work by being credible rather than by being fully used. The Bank of England announced up to GBP 65 billion of capacity and needed only about 30% of it, because the announcement itself reduced the urgency of the fire sale.

Where it appears in the course

Think about it

- The pension schemes' overall funded position was improving throughout the crisis, yet some funds were forced sellers of gilts within days. What does that tell you about the difference between a solvency check and a liquidity check?

- The Bank of England announced up to GBP 65 billion of purchase capacity but used only about GBP 19.3 billion. Why might announcing a large backstop reduce the amount a central bank actually has to spend?

- If UK pension schemes had hedged their interest-rate risk without any leverage, buying only as many long gilts as their capital allowed, how would the events of September 2022 have played out differently for them, and what would they have given up by hedging that way?

Sources

- Jon Cunliffe (Bank of England Deputy Governor for Financial Stability), letter to the Treasury Select Committee, 5 October 2022, via UK Parliament Treasury Committee publications, committees.parliament.uk.

- Bank of England, Market Notice, "Gilt Market Operations," 28 September 2022, bankofengland.co.uk.

- Bank of England, "Statement on end of gilt market operations," 14 October 2022, and "Bank of England completes unwind of recent financial stability gilt purchases," January 2023, bankofengland.co.uk.

- Bank of England, Quarterly Bulletin 2023, "Financial stability buy/sell tools: a gilt market case study" (Paul Alexander, Rand Fakhoury, Tom Horn, Waris Panjwani, Matt Roberts-Sklar), bankofengland.co.uk.

- Sarah Breeden (Bank of England Executive Director for Financial Stability), "Risks from leverage: how did a small corner of the pensions industry threaten financial stability?", speech at ISDA/AIMA/Bank of England event, 7 November 2022, bankofengland.co.uk.

- Carolyn A. Wilkins (Princeton University and Bank of England), "Financial Stability and Monetary Policy: Lessons from the UK's LDI Crisis," Griswold Center for Economic Policy Studies Working Paper No. 336, Princeton University, August 2024, gceps.princeton.edu.

- Central Bank of Ireland, Financial Stability Note, "Irish-Resident LDI Funds and the 2022 Gilt Market Crisis," 2023, centralbank.ie.

- Institute for Fiscal Studies, "Mini-Budget response," 23 September 2022, ifs.org.uk; House of Commons Library, briefing CBP-9624, "September 2022 fiscal statement: A summary," commonslibrary.parliament.uk.

- PPF 7800 Index, Pension Protection Fund, monthly updates including the December 2022 figure of a 136.5% funding ratio, ppf.co.uk.

- Contemporaneous press corroboration: CNBC, "UK PM Liz Truss fires Finance Minister Kwasi Kwarteng," 14 October 2022; Washington Post, CNN and NPR, 20 October 2022, on Liz Truss's resignation.